Tags

Financial Systemic Issues: Booms and Busts - Central Banking and Money - Corporate Governance - Cryptocurrencies - Government and Bureaucracy - Inflation - Long-term Economics - Risk and Uncertainty - Retirement Finance

Financial Markets: Banking - Banking Politics - Housing Finance - Municipal Finance - Sovereign Debt - Student Loans

Categories

Blogs - Books - Op-eds - Letters to the editor - Policy papers and research - Testimony to Congress - Podcasts - Event videos - Media quotes - Poetry

The Federal Reserve is the bank most in need of a stress test

Published in Real Clear Markets.

Do you know a bank that is leveraged at more than 100:1-to be exact, with assets of 111 times its equity? You do: it’s the Federal Reserve.

The consolidated Federal Reserves banks had total assets of $4.47 trillion as of Dec. 14, 2016, compared to total capital of merely $40.4 billion, or less than 1 percent of assets-actually, 0.9 percent.

The largest Federal Reserve Bank by far, New York, sports $2.47 trillion in total assets and only $13 billion in total capital, for leverage of a pretty remarkable 190 times and a capital ratio of 0.53 percent.

The Fed enjoys imposing stress tests on everybody else. What if we give the Fed a stress test? The interest rate risk of the Fed is similar to a 1980s savings-and-loan – lots of long-term, fixed rate assets, with short funding. So let’s apply a simple and standard interest rate stress test. Suppose long-term interest rates rise by 2 percent, to a historically more normal level. What happens to the Fed?

Well, the Fed now owns $4.4 trillion of long-term, fixed-rate assets and unamortized premium paid. It does not disclose the duration of this massive position, but let’s say it’s five years (it could be longer). If interest rates rise by 2 percent, the market value loss to the Fed is approximately 5 times 2 percent or 10 percent of the $4.4 trillion position. That would be an economic loss of $440 billion. That is 11 times the Fed’s total capital.

It seems highly likely that the Federal Reserve System, and the Federal Reserve Bank of New York in particular, would then be hugely insolvent on a mark-to-market basis. Stress test score: F.

Defenders of the Fed confidently claim that it doesn’t matter if the Fed is insolvent. Maybe they are right. If they are, the Fed should have no hesitation at all in publishing the mark to market of its giant securities portfolio, the way the Swiss central bank is required to do. To the Fed Board of Governors: How about it?

The housing bubble renewed?

Published by the R Street Institute.

Average U.S. house prices are back over their 2006 bubble top, as measured by the Case-Shiller Home Price Indices. “Home Prices Recover Ground Lost During Bust” read the Wall Street Journal headline.

But these prices are in nominal dollars, not inflation-adjusted dollars. While the Federal Reserve assures us that inflation is “low,” it tirelessly works to depreciate the dollar. Over the decade since the housing bubble peak, aggregate inflation has been 19 percent, so 2016 dollars are worth 84 cents compared to 2006 dollars.

House prices since 1987 in nominal terms look like this:

In inflation-adjusted terms, the chart is different. Average house prices in real terms are indeed very high, but still 16 percent below their bubble top. They have reached the level of March 2004, when the bubble was well advanced into exuberance, but not yet at its maximum. It had made about 54 percent of its 1999-2006 run.

From 1999 to 2004, real house prices increased at an average rate of 7.2 percent per year. In our renewed house price boom from 2012 to now, real prices have increased at 6.6 percent per year—pretty similar.

All this is depicted in Chart 2:

The Federal Reserve had reduced short-term interest rates to very low levels in 2001 to 2004, which fed the bubble. In 2004, it started to raise them. The house price run up since 2012 has also been fed by extremely low interest rates. Now the Fed must raise rates again and is getting ready to do so. Long-term mortgage interest rates have already increased sharply.

Should being back to 2004 in real terms worry us? Yes.

Household incomes can fall even when everyone’s getting richer

Published by the R Street Institute.

One of the politically hottest statistics right now is median household income, especially its slow growth. But there is a big problem with understanding what this statistic means, since it mixes up two different things: the changing composition of households and changes in incomes. If the makeup of households is altering dramatically, as it has in recent decades, median household income may be a quite misleading number.

For example, it is mathematically possible for everyone’s income to be rising, while the median household income is falling. How is that possible? The paradox is caused by counting by households, when the relationship between individuals and households keeps shifting.

To take the simplest possible case: Consider a population of one household, a married couple, each of whom has an income of $50,000. The median household income is $100,000. Their incomes each rise by 10 percent to $55,000—but they get divorced. Now there are two households. The median household income has become $55,000. The median household income has gone down by 45 percent! Obviously, we have a demographic event, not an income event.

Suppose our married couple stays married with their new household income of $110,000. An immigrant joins the population, making $20,000, which is three or four times his previous income. In this case, the median household income has become $65,000, falling 35 percent! But everybody is better off than they were before.

In what is naturally a more complicated way, just these sorts of major changes have been going on inside the statistics that count income by household. If the composition of households were unchanged, the statistics would be more straightforward. But this is obviously not the case. Until the demographic changes are untangled from the results, it’s not clear what the changes in median household income tell us.

The Fed should be accountable for its results

Published in The Wall Street Journal.

“Vote Brings Uncertainty for Fed” (U.S. News, Nov. 10) says that President-elect Donald Trump might work with Congress to rewrite the laws governing the Fed’s structure. Good idea. It is of course decried by the Federal Reserve as a threat to its independence.

We should hope that the new president does proceed with this project. The Fed needs to be made accountable, as every part of the government should be. The notion that any part of the government, especially one as powerful and dangerous as the Fed, should be granted independence of checks and balances is misguided. Naturally, all bureaucrats resent being subject to the elected representatives of the people, but this doesn’t exempt them from their democratic accountability to the legislature that created them and may uncreate them.

The Fed is still carrying out emergency monetary experimentation seven years after the end of the crisis. It is busy robbing savers to benefit borrowers and leveraged speculators—a political act. It is imperative to figure out how best to make the Fed accountable to the Congress and to correct the evolved imbalance between its power and its accountability.

GDP per-worker vs. GDP per-capita

Published by the R Street Institute.

We have previously compared the growth in real per-capita gross domestic product between the United States and Japan and among the 10 largest advanced economies. Growth in GDP per-capita measures the increase in the average economic well-being in the country, and adjusts gross GDP growth for whether the population is increasing, stable or declining.

We now shift to comparisons of growth in GDP per-worker (more precisely, per employed person). This addresses productivity, rather than overall economic well-being, and adjusts for shifts in the composition of the population among those who are employed. Those are who not employed include, for example, children, full-time students, retired people, those unemployed and looking for work, those unemployed and not looking for work, and those (especially mothers) who do plenty of work in the home, but not as paid employees.

If the overall population is growing, it’s possible for GDP to grow while GDP per-capita does not. Similarly, if there is a shift within the population toward greater workforce participation, GDP per-capita might grow, while GDP per-worker does not. More generally, the growth rates of these measures of economic performance may be quite different.

Table 1 compares the striking slowdown in economic growth between the last half of the 20th century and the first 15 years of the 21st in the growth of real GDP, both per-capita and per-worker. However, the 21st century slowdown, while marked, is less extreme when measured per-worker (1.82 percent to 1.11 percent) than when measured per-capita (2.25 percent to 0.90 percent). In other words, the productivity slowdown is less than the overall economic welfare deceleration. This reflects demographic changes: from 1959 to 2000, the number of workers grew faster than the population as a whole. In the 21st century, it’s grown more slowly.

How does the United States compare to Japan, when measured in growth in real GDP per-worker? Here our data makes us shift to 1960 to 2014, still a more than 50-year run. The relative growth performance of the two countries flips dramatically between the 20th and 21st centuries, although both are significantly slower, as shown in Table 2. Japan will continue to be an interesting case of a very technically advanced, but rapidly aging economy with falling employment and a falling population going forward.

Seemingly small differences in compound growth rates make for big differences if they continue over time. Table 3 shows the multiple of real GDP per-worker over 50 years in the actual second half of the 20th century, compared to a projection for 50 years of the 21st century if the century’s current trends continue. The result is a drop from an aggregate improvement of 2.5 times, to 1.7 times.

Can the growth in real GDP per-worker reaccelerate or not? That is indeed the question.

Letter to Oversight Board of Puerto Rico

Published by the R Street Institute.

In response to your request for public comments on the draft Puerto Rico fiscal plan, I respectfully submit the following thoughts.

An old friend of mine who ran a publishing company was famous for returning manuscripts to hopeful authors with this note written at the top: “OK to revise.” This is my summary view of the draft plan for three reasons:

The recent elections in both Puerto Rico and the United States resulted in changing both administrations. Presumably a new governor and new members of the U.S. Treasury Department will have different or additional positions to explore.

The draft plan entirely sidestepped the critical question of how to approach the debt restructuring obviously required.

The draft plan likewise sidestepped the essential questions about how to address the insolvent public-pension plans of Puerto Rico.

However, parts of the draft plan should, in my opinion, enter into final form and implementation as rapidly as practicable. These are the programs to improve budget controls, financial reporting, rationalization of expenditures, effectiveness of tax collections and, in general, all programs to promote stronger financial management and financial integrity. It seem to me that these should be put into a separate plan document for individual and expedited consideration.

To these essential programs should, in my opinion, be added the creation of a chief financial officer for Puerto Rico, closely modeled on the very successful Office of the Chief Financial Officer of Washington, D.C., which was one of the key reforms under its Financial Control Board in the 1990s.

It would be a pleasure to provide any other information which might be useful.

Yours respectfully,

Alex J. Pollock

Chapter 11 for Social Security?

Published in Barron’s.

In their Other Voices essay, Dudley Kimball and Robert Morgan said that Social Security will be insolvent in 2034.

In the sense of having liabilities vastly greater than assets, it is deeply insolvent today. Social Security really needs the equivalent of a Chapter 11 bankruptcy reorganization.

Life expectancy for 20-year-old white men in the 1930s was 66—meaning that, on average, he’d get one year of Social Security. Today, a 20-year-old man has a life expectancy of 82.

Social Security has become a complex mix of financial functions. It is partly a welfare program; Kimball and Morgan would make it more so. It is partly a forced savings program with a very low average rate of return. It is partly insurance against outliving your savings. And it is entirely broke in present-value terms, reflecting cash already paid to those who took out much more than they put in.

It is time to draw a line and have a reorganization. Those people who can easily afford it could take substantial haircuts on their future benefits, receiving say 60 cents to 70 cents on the dollar, in exchange for voluntarily opting out of the program. This would make Social Security much less insolvent.

For the other creditors, Congress should step up, write off the Treasury’s loss, put in whatever it takes to pay off the accrued benefits at par, and put Social Security into runoff. To this extent, the government would then have honest, as opposed to dishonest, books. A program designed for the now-irrelevant demographics of the 1930s would slowly liquidate.

Then a sound retirement finance program could be put in place to go forward, based on 21st century demographics. Doubtless, the politics would be interesting. But perhaps starting over offers a better chance than trying to remake the 1930s DC-3 of Social Security into a jumbo jet while it’s flying.

Why current asset prices are dangerously exaggerated

Published in Real Clear Markets.

Over the long term, real per-capita household net worth in the United States has grown at about 2 percent a year. This is a wonderful achievement of the enterprising economy.

In shorter periods, when asset prices get inflated in a bubble, household per-capita wealth appears to rise notably above this long-term pace, but ultimately, bubble asset prices inevitably shrivel. When they do, many commentators claim that a lot of “wealth” been lost by households. It hasn’t, because the apparent wealth was not really there in the first place: it was an illusion of the bubble.

If any very great number of people try to sell out at the bubble prices, the evanescent “wealth” disappears, the bubble deflates and the long-term trend reasserts itself, so the aggregate bubble prices can never be realized. Bubble times reflect what Walter Bagehot so truly wrote in 1873: “All people are most credulous when they are most happy.”

Graph 1 is the record of 1953 to 2016. The temporary illusion of wealth represented by two remarkable bubbles of recent decades is obvious.

We should recall with amused irony that the central bankers formerly congratulated themselves for creating what they credulously called “The Great Moderation.” What they actually presided over was the Era of Great Bubbles: first the Great Overpaying for Tech Stocks in the 1990s, then the Great Overleveraging of Real Estate in the 2000s.

And now? They are congratulating themselves again for innovative or radical monetary actions, including their zero interest rate policy (ZIRP), which expropriates the returns to savers and makes the present values of assets rise. Many observers, including me, think they have by their manipulations inflated new bubbles in stocks, bonds and houses. This has put real household wealth per-capita measured at current asset prices back over its 2 percent growth line, although not as egregiously as in the government-promoted housing bubble of the last decade. We can expect ultimate regression to the trend, as always.

But has the trend shifted? From 1950 to 2000, growth in U.S. real per-capita gross domestic product averaged more than 2 percent per-year. This is consistent with a 2 percent growth in wealth per-capita. But since 2000, real per-capita GDP has grown less than 1 percent per-year. Suppose the stagflationists are right, and this represents not a temporary, but a sustained downshift. Then it would be consistent with real per-capita economic growth to move our trend growth in real net worth per-capita down to 1 percent. Graph 2 shows the possible new trend line, starting in 2000.

If we measure from this new line, the current ZIRP bubble looks much worse; it has reached almost the same magnitude as the infamous housing bubble of a decade ago.

Graph 3 shows the variation from the 2 percent and 1 percent lines, displaying the illusory household wealth effects of the series of bubbles in a different fashion.

The more you believe the stagflationist theory, the more you must conclude that current asset prices are dangerously exaggerated, the greater the bubble you must conclude that the central bank experiments have wrought and the further we have to fall back to the trend.

Growth in per-capita GDP: How does the United States rank?

Published by the R Street Institute.

Growth in gross domestic product after adjustment for inflation (real GDP) is the most frequently reported and discussed economic measure. More important, however, is how people on average are doing from an economic standpoint. This means measuring output per person, or real per-capita GDP, and its growth rate.

How does the United States rank among other countries on this growth measure?

In “Japan vs. the U.S. in Per Capita GDP,” we observed that, for the 15 completed years of the 21st century, there is not much difference between average growth in real per-capita GDP between the United States and Japan—the latter often described as suffering from economic stagnation.

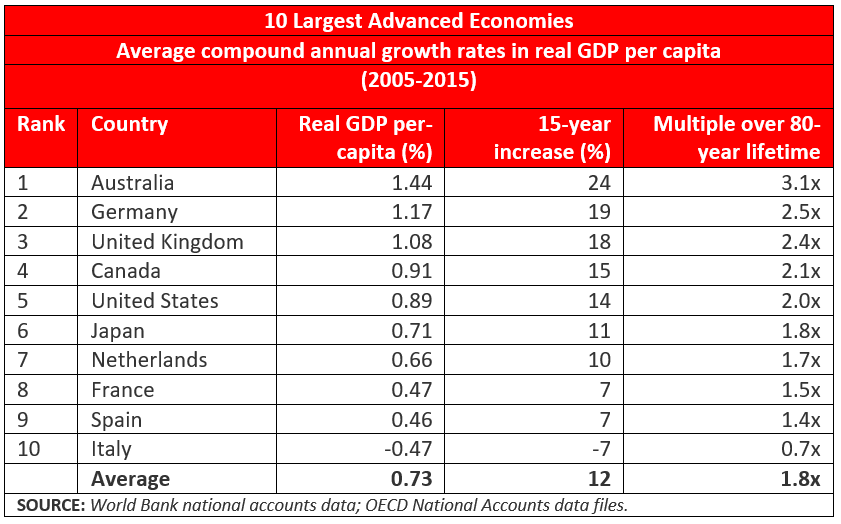

Now we expand our comparison to the 10 largest advanced economies in the world. Here they are, ranked by the average growth rate in real per-capita GDP in this century so far:

Note that the United States and Japan are together right in the middle of the pack, fifth and sixth, respectively, bracketed by Canada and the Netherlands. Three other countries achieved substantially higher real growth rates when measured per person, and three were substantially lower, including Italy, whose growth rate was negative. Among the 10 countries, the average growth rate was 0.73 percent per year, in between the United States and Japan.

The table also shows how much aggregate difference there is as the growth rate compounds for 15 years. At Australia’s leading 1.44 percent average growth rate, aggregate product per person increased by 24 percent in 15 years. The comparable number for the United States is 14 percent. France and Spain are half that at 7 percent and Italy is a 7 percent decrease.

The effects of differences in compound growth rates are always impressive if they continue over a long time.

We calculate what the aggregate increase in average economic well-being would be if the growth rate in real per-capita GDP could be sustained for a lifetime of 80 years. Australians would become, on average, three times better off during their lives; Canadians, Americans and Japanese about twice as well off. Spaniards would be 40 percent better off. In the long view of the millennia of human history, this is very impressive.

Of course, if the growth rate in real per-capita GDP could be 2 percent, these numbers would be much more impressive yet. Then, in an 80-year lifetime, the average economic standard of living would quintuple.

Homeownership Rates: It depends on whether you are married

Published by the R Street Institute.

The attached piece originally appeared in the Autumn 2016 edition of Housing Finance International.

American political rhetoric endlessly repeats that homeownership is part of the “American Dream.” So it is for most people, especially if you are married, as we will see.

As part of promoting this “dream,” the U.S. government has for many years created large subsidies for mortgage borrowing and huge government-sponsored financial institutions to expand mortgage lending. Most notable among these are Fannie Mae and Freddie Mac, which notoriously went broke in 2008 while following the government’s orders to make more so-called “affordable” loans, and survived only thanks to a $189 billion taxpayer bailout.

Fannie and Freddie are still massive operations, featuring a combined $5 trillion in assets (that’s trillion with a “T”), equity capital that is basically zero and utter dependence on the credit of the U.S. Treasury.

Given these massive and extremely expensive efforts, how has the American homeownership rate fared? Let us look back 30 years to 1985, and compare it to 2015. Thus we can go past the housing bubble and collapse of the 2000s, as well as past the financial collapse of the savings and loans in the late 1980s, and observe what has happened over a generation.

Read the rest.

Fed’s mandate is to ensure stable prices

Published in the Financial Times.

Sir, Michael Brownrigg (Letters, Oct. 4) makes a common, but fundamental, mistake in claiming that the Federal Reserve’s mandate includes “low inflation”. To the contrary, in the governing statute, Congress instructs the Fed to pursue “stable prices” not low inflation. Public confusion is understandable, since the Fed endlessly recites the oxymoron that “stable prices” means perpetual inflation (at the rate of 2 percent).

Mr Brownrigg is correct that there is no statutory instruction to the Fed to treat everybody equally. This does not change the egregious fact that the Fed has engineered a massive wealth transfer from savers to borrowers and leveraged speculators. To take a lot of money from some people and give it to others is a quintessentially political act. To whom is the Fed accountable for it?

‘Fin’ versus ‘tech’ in fintech

Published by the R Street Institute.

Financial technology – or “fintech,” in the modern parlance – may be seen as trendy, but computing technology has strongly influenced banking and finance for decades. Its effects include the creation of general-use credit and debit cards, going back to the 1950s, which we now take for granted worldwide; ATMs available any time and almost anywhere, going back to the 1970s; and the data capabilities that make structured mortgage-backed securities possible, going back to the 1980s.

Visa and MasterCard are considered leading fintech companies, which they are. Former Federal Reserve Chairman Paul Volcker once cynically remarked that ATMs were the only real financial innovation of recent times. Meanwhile, MBS vividly display the double potential of innovation, first for growth and then for disaster.

Investment banker J. Christopher Flowers has expressed the view that the current fintech boom will “leave a trail of failed companies in its wake.” Of course it will, just like the hundreds of automobile companies that sprang up a century ago or the myriad dot-com companies that mushroomed in the 1990s. The automobile and the internet were both society-changing innovations and the hundreds of failures are how we discover which are the truly valuable ideas and which aren’t. To paraphrase Friedrich Hayek’s memorable essay, competition is a discovery procedure.

Over time we will find out which innovations are real and which are mere fads. A key distinction in fintech, as in the financial world in general, is between those changes that make transactions faster, cheaper, more mobile and less bothersome (the “tech”), on the one hand; and those that make it easier to make loans and take credit risk (the “fin”), on the other. The former are likely to yield some truly useful innovations; the latter, which require lending people money that you hope they will pay back on time and with interest, is an old and tricky art. It is much easier to fool yourself about whether you are actually improving lending, as compared to technology.

Consider the idea of “lending money over the internet.” The “internet” part may invent something faster, cheaper and easier—just like the ATMs Volcker touts. The “lending money” part may be simply a new name for making bad loans, just as the dark side of MBS turned out to be.

So on one hand, we may have real innovation and progress, and on the other, merely endless cyclical repetition of costly credit mistakes. For example, the fintech firms LendingClub and OnDeck Capital presently find their stock prices about 80 percent down from their highs of less than two years ago, as they learn painful lessons about the “fin” part of fintech.

Nor is this distinction new. As James Grant, the acerbic and colorful chronicler of the foibles of financial markets, wrote in 1992:

In technology, therefore, banking has almost never looked back. On the other hand, this progress has paid scant dividends in judgment. Surrounded by computer terminals, bankers in the 1980s committed some of the greatest howlers in American financial history.

So they did, and more than 2,800 U.S. financial institutions, their growing computer power notwithstanding, failed between 1982 and 1992.

Bankers in the 21st century – avidly using vastly greater technological prowess, supplied with reams of data, running complex computer models to measure and manage (or so they thought) their credit risks – made even more egregious mistakes. As we all know, they created an amazing credit bubble and came close to tanking the entire financial system. Did the technology help them or seduce them?

Mathematicians and physicists – the “rocket scientists,” as they were called – had brought their impressive computer skills to Wall Street to help apply technology to mortgage finance. In the memorable summary of George Mason University’s Tony Sanders, “The rocket scientists built a missile which landed on themselves.” The mistakes were in the “fin” part of this effort, not the “tech” part.

In every financially trendy boom, we hear a lot about “creative” new financial products. A painful example was the homeownership strategy announced with fanfare by the Clinton administration in the 1990s. It called for “creative” mortgages, which turned out to mean mortgages likely to default.

Such products, no matter how much innovative computer technology surrounds and helps deliver them, are not real financial innovations. They are merely new ways to lower credit standards, run up leverage and increase old risks by new names. They are thus illusory financial innovations. As also pointed out by James Grant, science is progressive, but credit is cyclical.

Real innovations turn ideas into institutions which endure over time, various mistakes notwithstanding, as credit cards, ATMs and MBS have. Illusory innovations cyclically blossom and disappear. Both produce uncertainty, and uncertainty means we cannot know the future, period. We will continue to be surprised, positively and negatively, by the effects of financial innovation.

In short, financial markets are always in transition to some new state, but only some of this is progress. The rest is merely cyclical repetition. What is fintech? Doubtless, it is some of both.

Happy birthday, TARP!

Published by the R Street Institute.

Today, Oct. 3, is the eighth anniversary of congressional passage of the act that created the famous or notorious $700 billion bank bailout program in the midst of financial panic of late 2008. In case you have forgotten, TARP stood for the Troubled Asset Relief Program, and the authorizing legislation was the Emergency Economic Stabilization Act of 2008. An emergency it was, with one failure following fast on another.

Eight years on, when we know that the panic passed, when house prices are booming again, when the stock market is high and life has gone on, it’s hard to recreate psychologically the uncertainty and fear of that period. Memories naturally lose their vividness and then fade altogether, making the next cyclical bust more likely.

The design of TARP originally was to quell the crisis by having the U.S. Treasury buy depreciated mortgage-backed securities from banks, removing these “troubled assets” from private balance sheets and thus giving them “relief.” When this was proposed, it was already clear that it was not going to work. The crisis had created insolvencies, with deficit equity capital. By buying assets from banks so they realized big losses, you were not going to fix their capital. Neither would lending them more money from the Federal Reserve fix their capital: if you are broke, no matter how much more you borrow, you are still broke.

By September 2008, the British government already had decided it had to make equity investments in insolvent banks. This replicated the U.S. experience of the 1930s, when the Reconstruction Finance Corp., originally set up to make loans to troubled banks, realized it had to make equity investments instead, in the form of preferred stock. It also replicated the experience of Japan in the 1990s. As TARP was being debated, it seemed to me that the equity investment model was better than the proposed TARP design, and so it proved to be. The RFC overall made a profit on its bank investments, and so, as it turned out, did TARP.

But what Treasury Secretary Henry Paulson had told Congress in getting the legislation passed was that they were approving a program for buying mortgage securities. However, as Paulson revealed in educational crisis memoir “On the Brink,” even as these arguments were being made:

Ben Bernanke had told me that he thought that solving the crisis would demand more than the illiquid asset purchases we had asked for. In his view, we would have to inject equity capital into financial institutions.

Bernanke was right about that, but Paulson thought “we would sabotage our efforts with Congress if we raised our hands midstream and said we might need to inject equity.” Well, you can’t tell the elected representatives of the people what is really going on. When the act did get passed and signed into law Oct. 3, says Paulson: “I made sure to tell…the team: ‘Figure out a way we can put equity in these companies.’” And so they did.

Shortly thereafter, Paulson reflects, “I began seriously to doubt that our asset-buying program could work. This pained me, as I had sincerely promoted the purchases to Congress and the public as the best solution” and “dropping the asset-buying plan would undermine our credibility.” Instead, TARP proceeded by making equity investments in preferred stock.

By now, the TARP investments in banks are almost entirely liquidated at a profit to the Treasury. The program went on to make losing investments in the bailouts of automobile companies (which equally were bailouts of the United Automobile Workers union) and to spend money not authorized by statute on programs for defaulted mortgages. All in all, Oct. 3 launched a most eventful history.

“I had expected [TARP] to be politically unpopular, but the intensity of the backlash astonished me,” wrote Paulson.

Its birthday is a good time to reflect on TARP and try to decide what you would have done in Secretary Paulson’s place, had you been handed that overwhelming responsibility.

The Credit Crunch of 1966: An instructive 50th anniversary

Published in Real Clear Markets.

It’s the 50th anniversary of the Credit Crunch of 1966, which roiled financial markets in August and September of that year. Group financial memory fades, so if you don’t know or remember that there was such a crunch, searing at the time, you are not alone. Yet it taught an essential lesson, again being relearned right now, 50 years later: the Federal Reserve, and central banks in general, simply do not know what the right interest rate is.

Central to the events of 1966 was that the Federal Reserve set the maximum interest rates that banks could pay on their deposits. This was the Fed’s now long-gone but then critical “Regulation Q” authority, at the time considered an essential part of the banking system.

As of July 1966, the Fed had set the interest-rate ceiling on savings deposits at 4 percent. For so-called “multiple maturity” time deposits (where withdrawal was at the depositor’s notice) it was 4 percent for a minimum maturity of up to 89 days, and 5 percent for 90 days or more. For fixed-maturity date time deposits, the ceiling was 5.5 percent. In September 1966, it dropped to 5 percent, except that deposits of more than $100,000 (that’s $743,000 in 2016 dollars) could still get 5.5 percent.

How did the Fed know those numbers were right? It didn’t, as events demonstrated. Most of the time over the preceding decades, they had set the ceiling over market rates, so it generally hadn’t been an issue.

But in 1966, there was strong credit demand from an extended economic expansion, plus inflationary pressure from the Vietnam War and “Great Society” deficits. Interest rates in the open market went much higher than before. Three-month Treasury bill yields got to 5.59 percent, the federal funds rate to 5.77 percent and commercial paper rates to 6 percent. Market rates on negotiable CDs went over the ceilings. “The prime rate briefly reached the then unheard of level of 6 percent,” wrote economist Albert Wojnilower. A 6 percent prime rate was the highest it had been in more than 30 years.

This time, the Fed refused to raise the ceiling in line with the market, in part reflecting political pressure to limit competition for deposits in order to favor savings-and-loan institutions, which were stuck with long-term mortgages at low fixed rates. Lending long and borrowing short was already dangerous in 1966.

Naturally, in response, people took their money out of both banks and savings and loans and put it into higher-yielding conservative investments, a perfectly sensible thing to do. This process had a cumbersome name at the time: “disintermediation”—a problem created entirely by regulation. Unable to expand their funding, the banks cut back on their loans. The savings and loans cut way back on their mortgage loans. “For most people, residential mortgage money was unobtainable…there was a sharp slump in mortgage loans and housing starts,” wrote The New York Times.

Banks also cut back on their previously expanding investments, notably in municipal bonds. Both banks and thrifts worried about their ability to fund their existing balance sheets. As described by the theoretician of financial crises, Hyman Minsky: “By the end of August, the disorganization in the municipals market, rumors about the solvency and liquidity of savings institutions, and the frantic [funding] efforts by money-center banks generated what can be characterized as a controlled panic.” Not allowed to bid competitive rates for deposits, as the St. Louis Fed’s history of the credit crunch reports: “Banks had never before experienced a large outflow of time deposits.”

So the Fed fixed prices and the result was the credit crunch. Following Wojnilower’s lively account: “Lending to all but the most established and necessitous customers was halted abruptly. Chief executives of leading banks reportedly were humbled to the point of pleading with their counterparts in industry to renew their CDs.” Further, in order to the raise needed funds, there was “the apparent inevitability of massive distress sales of long-term assets into a paralyzed marketplace.”

Who came to the rescue? The cause of the problem. “The gravity of the situation penetrated to an initially incredulous Federal Reserve,” Wojnilower continues. Banks were invited to borrow at the discount window in the face of “the very lively fears that major banks might have to close their doors.”

The shock of the credit crunch led the Fed into “a long-lasting series of private and public reassurances that no such crisis would ever be permitted to recur.” How did that work out? Three years later came the more severe credit crunch of 1969. As economist Charlotte E. Ruebling wrote at the time, “market interest rates have soared to levels never before reached in this country,” but “rates on deposits at banks and other financial institutions have been held much lower.” By the Fed, of course.

The authors of Regulation Q had a really bad idea, based on the false assumption that the Fed would somehow know the right answer. But the Fed did not know what the right interest rate was in 1966, or 1969—nor do they know it now. They never have and cannot know it. Put not your faith in their dubious “expertise.”

Negative rates aren’t working. Why do central banks persist?

Published in Real Clear Markets with Paul Kupiec.

Monetary policies in Europe and Japan have produced trillions of dollars of bonds with negative nominal interest rates in the hope of stimulating economic growth. Indeed, the Bank of Japan’s recent policy announcement doubles-down on this strategy by pledging to cap 10-year Japanese government bond yields at zero until the central bank hits its 2 percent inflation target.

But there is little evidence that negative interest rates are stimulating economic growth. Economic data suggest that consumers are actually saving more in countries with negative interest rates. And business investment, far from being stimulated by near-zero borrowing costs, is weak across the board. It’s time for a critical reassessment of unconventional post-crisis monetary policy experiments.

A typical consumer’s lifecycle has three phases – a borrowing phase, a saving phase and a phase for consuming savings in retirement. The aging of developed countries has increased the economic importance of the latter two lifecycle phases. While negative real interest rates benefit borrowing households, they are a tax on savers and those in retirement.

With negative nominal interest rates, prudently sock away your income for years and you are certain to receive less money than you invested. On top of that, monetary authorities worldwide target perpetual inflation, so chances are that you will face a higher price level in the future. Faced with this double whammy, economists predict that consumers should spend rather than save, but the data strongly suggest that households are compensating for negative interest rates by saving more, not less.

Recent OECD data show that, as average short-term interest rates turned negative, household savings rates increased in Switzerland, Germany, Sweden, Denmark and Japan. The OECD forecasts decade-high household savings rates in 2016 for all these countries except Japan.

Recent negative and near-zero interest rate policies have also had unanticipated impacts on business investment. If businesses followed economic textbooks, they would invest in activities that are profitable when expected revenues and costs are discounted using their average cost of funds. Under this decision rule, investment should increase when monetary policies force interest rates to zero or below, because more investments are profitable when a business’ cost of borrowing falls.

But many business mangers apparently skipped this economics lecture. Research has shown that many firms evaluate investments by discounting future cash flows using a management-set hurdle rate, not their firm’s cost of raising new funds. Survey evidence finds that firms set investment hurdle rates between 12 to 15 percent for investments similar to their existing business lines, and significantly higher for new business ventures.

Moreover, the evidence from multiple countries suggests that business hurdle rates are “sticky” over time. Firms do not appear to adjust their hurdle rates in response to changes in short-term interest rates. For example, a recent Federal Reserve Board study concludes that business investment hurdle rates have changed little since the 1980s, despite nearly double-digit declines in corporate borrowing costs.

The missing piece in the business investment puzzle is uncertainty. When businesses perceive high downside risks, they wait to invest. The delay allows firms to acquire new information and avoid potential downside losses by postponing investing until the data confirm an improved outlook. This behavior mimics the Federal Reserve and other monetary authorities’ habit of delaying action until additional data confirm the underlying economic trend.

The option to wait has the potential to put a huge drag on business investment. When monetary authorities use highly publicized, radical approaches like QE and negative interest rates and justify the policies as “insurance” against a deflationary spiral, they are themselves creating uncertainty. The more monetary authorities push the negative interest rate frontier to save their economies from disaster, the bigger the uncertainty they telegraph to businesses and consumers about downside risks.

Against mounting evidence, it is becoming harder to cling to the theory that near-zero and negative interest rates stimulate economic growth. When rates are negative, savers appear to save more, not less; retirees consume less to conserve their nest eggs; and business investment stagnates, as the value of the option to wait for an improved economic outlook grows.

But near-zero and negative interest rates do have one beneficiary – governments. Near zero and negative nominal rates reduce budget deficits because governments borrow virtually for free or even get paid to issue debt. So although near-zero and negative interest rates cloud the outlook for economic growth, these monetary policies have provided a silver lining for treasuries and finance ministries.

Taking on Leviathan

Published in the Thomas Hobbes (1588-1679), the great philosopher of the authoritarian state, in a famous metaphor portrayed the government as a dominating giant or Leviathan, animated by absolute sovereignty, and passing out rewards and punishments as it saw fit. It alone could control the unruly passions of the people and create stability and safety.

Today’s “administrative state”—or government bureaucracy, acting simultaneously as sovereign legislator, executive, and judge—brings Hobbes’ image of the giant vividly to mind.Nowhere is his metaphor more apt than in the government’s attempts at “systemic financial stability.” Hobbes’ 21st century acolytes include former Senator Chris Dodd (D-Conn.) and former Congressman Barney Frank (D-Mass.), whose Dodd-Frank Act sought to prevent financial crises, as Hobbes sought to prevent civil wars, by enlarging the giant. Now, as then, how to control the unruly passions, lust for power, and misguided enthusiasms of the state itself is left unanswered.

However, Congressman Jeb Hensarling (R-Tex.), who chairs the House Financial Services Committee, is now taking on Leviathan in the financial system with the proposed Creating Hope and Opportunity for Investors, Consumers and Entrepreneurs (CHOICE) Act. If it seems unlikely that he could fell the giant altogether, perhaps he could limit and better control and confine it, at least with respect to banking and the people’s money. If he succeeded, the federal government would place more emphasis on competitive markets and less on the diktats of the central bank and regulatory bureaucrats whom Dodd-Frank made sovereign.

Writing his book Leviathan in 1651, in the wake of the English Civil War and the beheading of King Charles I, Hobbes had this to say: “By art is created that great LEVIATHAN called a COMMONWEALTH or STATE (in Latin, CIVITAS), which is but an artificial man, though of much greater stature and strength.”

He went on:

sovereignty is an artificial soul, as giving life and motion to the whole body; the magistrates and other officers of judicature and execution, artificial joints; reward and punishment (by which fastened to the seat of the sovereignty, every joint and member is moved to perform his duty) are the nerves.

Moreover,

Salus Populi (the people’s safety) its business; counsellors, by whom all things needful to know are suggested unto it, are the memory; equity and laws, an artificial reason and will; concord, health; sedition, sickness; and civil war, death.

Writing four decades before the founding of the Bank of England, Hobbes can be forgiven for not mentioning the central bank, which has since become a key element of sovereignty. We need to extend his metaphor to include it. We could say that the central bank is a kind of artificial heart pumping the circulating blood of credit and money, making sure to lend the government as much as it wants. It often pumps this blood of credit to an excessive extent, causing financial markets to inflate, be overly sanguine, then bust, constrict their flows and suffer the heart attacks of financial panics.

Three centuries or so after Hobbes, Leviathan developed a new capability: that of constructing vast shell games guaranteeing huge quantities of other people’s debt and taking vast financial risks, while pretending that it wasn’t doing this, and keeping this debt off the books. I refer to the invention of government-sponsored enterprises like Fannie Mae and Freddie Mac, and to related schemes such as government-sponsored insurance companies, like the Federal Savings and Loan Insurance Corporation and the Pension Benefit Guaranty Corporation. All serve as Leviathan’s artificial stomach and gluttonous appetite for risk, causing in time obesity, flatulence, indigestion, and finally the heartburn of publicly admitted insolvency.

Although financial panics temporarily render Leviathan stunned and confused, in short order it resumes its energetic activity and ambitious pursuit of greater power. Writing legislation in 2010, in the wake of the financial crisis of 2007 to 2009, Senator Dodd and Representative Frank ordered Leviathan to make deep expansions into the financial sector. The people’s financial safety and concord became defined as a new supreme demand for “compliance” with the orders of government bureaucrats, who were assumed to know the right answers.

The Dodd-Frank Act was passed in 2010 on party line votes at a time of insuperable Democratic majorities in both houses of Congress. Shortly after voting it in, the Democrats suffered stinging losses in that year’s congressional elections. No subsequent Congress would ever have dreamed of passing anything remotely resembling Dodd-Frank, but financial Leviathan had already been put on steroids and unleashed.

Now comes Chairman Hensarling to try to bring financial Leviathan back under control. The CHOICE Act would reform Leviathan’s activity in a wide swath of financial areas. It would:

Remove onerous Dodd-Frank burdens on banks that maintain a high tangible capital ratio (defined as 10 percent of total assets), thus creating a simple rule instead of the notoriously complex ones now in force.

Force the Financial Stability Oversight Council into greater transparency by cutting back the power of this committee of regulators to make opaque decisions in secret.

Correct the egregiously undemocratic governance of another bureaucratic invention, the Consumer Financial Protection Bureau, by giving it a bipartisan board and subjecting it to the congressional oversight and appropriations process that every federal agency should have.

Require greater accountability and transparency from Leviathan’s heart, the Federal Reserve.

Require cost-benefit analysis for new regulations and a subsequent measurement of whether they achieved their goals—imagine that!

Repeal the “Chevron Doctrine” that leads judges to defer to federal agencies. This is essential, as bureaucrats make ever-bolder excursions beyond their legal authority.

Take numerous steps to relieve Leviathan’s heavy hand on small businesses and small banks.

The CHOICE Act will likely be taken up by the House Financial Services Committee this fall—and be ready for further consideration if, as is forecast by most people, Republicans retain control of the House of Representatives in the upcoming election. The debates about the bill will be contentious and sharply partisan, with vehement opposition from those who love Leviathan. How far the reform bill can go depends on how other parts of the election turn out.

Will financial Leviathan grow ever fatter, more arrogant, and more intrusive? Or can it be put on a long-term diet by constraining its arrogance, correcting its pretensions, imbuing its artificial soul with behavior befitting a republic, and put in the service of a limited government of checks and balances?

The CHOICE Act is a good start at this daunting and essential project.

The new century brings remarkable downshift in per-capita GDP growth

Published in Real Clear Markets.

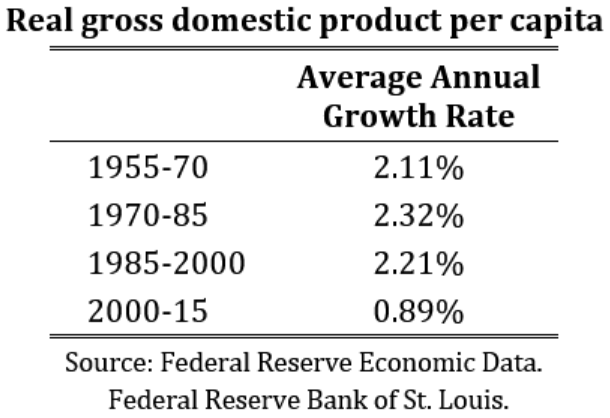

For the half-century from 1950 to 2000, U.S. real gross domestic product per capita grew at an average rate of 2.22 percent per year. For the first 15 years of the 21st century so far, this key measure of the overall standard of living has grown, on average, at only 0.89 percent.

Of course, a growth rate per person of 0.89 percent is still growth, and growth in output per person sustained over years is still a notable achievement of the market economy.

But the difference between growth rates of something over 2 percent and a little less than 1 percent is a very big deal. How much difference does that drop make, if it continues? Thanks to the always-surprising power of compound growth rates over time, the difference in the resulting long-term standard of living is huge.

In a lifetime of 80 years, for example, per capita GDP growth of 0.89 percent per year will double the economic standard of living-on average, people will become twice as well off as before. But with a growth rate of 2.22 percent, GDP per capita will more than quintuple in the same 80 years-people will be five times as well off. Such amazing improvement has actually happened historically beginning with the economic revolutions of the 19th century and continuing through the 20th. In 1950, U.S. real per capita GDP was $14,886 (using constant 2009 dollars). By 2000, it was $44, 721-thus 3X in 50 years.

The downshift of our new century is apparent when we look at the average growth rates in successive 15-year periods, as shown in the table.

Why the downshift and will it continue? The answer, as with so many things in economics, is that we do not know.

One theory now proposed is “secular stagnation.” This is not really so much a theory as giving a different name to slower growth rates. “Stagnation” was also a noted economic assertion in the 1940s– just before the postwar boom and on the verge of 50 years of solid growth. The great economist, Joseph Schumpeter, writing in 1949 on “modern stagnationism,” observed that “stagnationist moods had been voiced, at intervals, by many economists before.” Now they are being voiced again. They were always wrong before. Will they be right this time?

Among the factors we may speculate contribute to the markedly slower growth in real per capita GDP of this century are: the drag from financial crises and their resource misallocations; the aging of the population, with lower birth rates and long retirements; the fall in labor participation rates, so there are fewer producers as a percent of the population; the ever-more oppressive tangle of government regulations, so that “compliance” with the orders issued by bureaucrats becomes the top priority; and the massive monetary distortions of central banks, pretending to know what they are doing.

Can all this continue to suppress the underlying growth dynamic of scientific advance, innovation, entrepreneurship and enterprise of a market economy? Unless the government interventions get a lot worse (which they may!), I believe the current stagnationists will likely join their historical predecessors among the ranks of the false prophets. Let us hope so.

Economic reform for Puerto Rico

Published by the R Street Institute.

The attached letter was submitted to the Bipartisan Congressional Task Force on Economic Growth in Puerto Rico.

Among the most fundamental of Puerto Rico’s many economic problems is that it is “stuck in a monetary union with the United States” (as Desmond Lachman of the American Enterprise Institute has correctly characterized it). In this situation of being forced to use the U.S. dollar, the Puerto Rican economy is simply uncompetitive, but the use of exchange rate policies to improve competitiveness or cushion budget tightening’s impact on domestic demand is precluded.

This is the same massive problem that Greece had and still has from being stuck in the monetary union of the euro. With any external currency adjustment forbidden, all the adjustment falls on internal reduction of costs. As Greece demonstrates, this continues to be very difficult and daunting, both economically and politically. This is true even after its creditors have taken huge haircuts. Puerto Rico’s creditors will take big haircuts, too, but that won’t solve its ongoing lack of competitiveness or the impact of the required budget tightening.

The European Union leadership feared that Greece’s exit from the euro might set off the unraveling of their whole common currency project. In contrast, there is not the slightest possibility that whatever happens in Puerto Rico will affect the stability or dominant role of the U.S. dollar. Even in the Greek case, European policy makers did seriously consider a back-up plan for a paper currency to be issued by Greek banks which would certainly have depreciated against the euro.

Dr. Lachman argues that Puerto Rico “needs the boldest of economic programs.” My suggestion is that the Task Force should consider “thinking about the unthinkable,” and include in its work a study of the “outside the box” possibility of currency reform for Puerto Rico. This would involve creating a new Puerto Rican currency which would be considerably devalued with respect to the U.S. dollar, thus allowing external, not only wrenching internal, adjustment of Puerto Rico’s uncompetitive cost structures. There is plenty of precedent for such currency reform, although this case is certainly complicated by the status of Puerto Rico as a territory. Could a U.S. territory have its own currency? Why not?

In such a study, one would have to consider the balance sheets of all the Puerto Rican depositories and how they would be affected in detail by denomination in a new currency, how various contracts would be affected, how exchange between the new currency and other currencies would be introduced, whether a new Puerto Rican central bank would be established, and many other problems of transition and functioning, of course. Existing Puerto Rican government debt in U.S. dollars would not be subject to redenomination, but this debt, a growing amount of it in default, is going to have to be significantly written down in any case.

Does the current monetary union pose deep problems for Puerto Rico? Undoubtedly. Would it make sense to release Puerto Rico from being stuck in a monetary union in which it cannot compete? Possibly. Would this be better than the Greek model of forcing internal cost deflation while providing big external subsidies? Probably. It does seem sensible to take a serious look at the possibility of currency reform.

Thank you for the chance to comment on this critical issue. It would be a pleasure to provide any further information which might be helpful.

Japan versus the United States in per-capita GDP

Published by the R Street Institute.

We often see and hear in the media about the “stagnation” of economic growth in Japan. Let’s look at the numbers and see how Japan has done compared to the United States in the 15 years of the 21st century so far.

If we measure by growth in real gross domestic product (GDP), without considering changes in population, Japan’s economic growth is far behind that of the United States. From 2000 to 2015, its real GDP grew an average of 0.72 percent per year, while U.S. real GDP grew an average of 1.77 percent.

In average growth rates, more than 1 percent per year is a big difference, indeed, as it compounds over time. Over 15 years, this annual growth rate difference would add up to U.S. GDP being 30 percent larger, compared to 11 percent larger for Japan, a difference of 19 percentage points.

However, economic well-being is not measured by aggregate GDP, but by GDP per capita. The question is how much production there is per person. In this case, measuring per-capita growth gives us a very different outcome.

In 2015, Japan’s population was essentially the same as it was in 2000, with an average annual growth rate of 0.01 percent. The corresponding annual growth rate of the U.S. population was 0.87 percent. So the U.S. added 39 million more people over the period to provide for.

Thus real GDP growth per capita in Japan was 0.71 percent per year. In the United States, it was 0.89 percent – a much more similar number. The growth rate advantage over Japan, measured per capita, is reduced to a modest 0.18 percent.

If 0.71 percent growth is “stagnant,” what is 0.89 percent?

Iron Chancellor was a good actuary too

Published in the Financial Times.

Sir, “Retirement age for young Germans will have to rise to 69, central bank warns” (Aug. 16). That is a quite reasonable, even generous, retirement age if you are going to live to 85 or 90 or more.

Moreover, it would not be the highest retirement age Germany has had. When Otto von Bismarck introduced the first state pension scheme in the German Empire of 1889, the retirement age was set at 70! Needless to say, on average you were going to live many fewer years after 70 then than now. The Iron Chancellor knew what he was doing, actuarially speaking