The new century brings remarkable downshift in per-capita GDP growth

Published in Real Clear Markets.

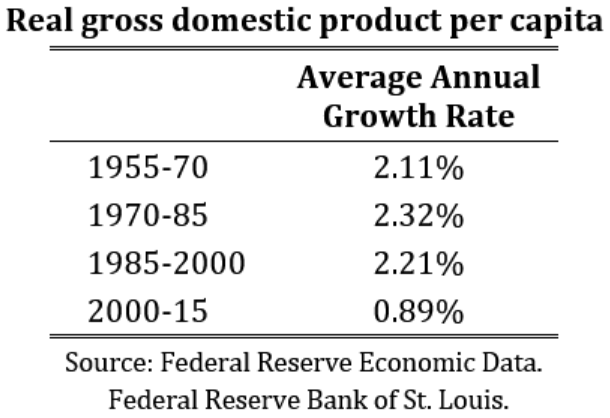

For the half-century from 1950 to 2000, U.S. real gross domestic product per capita grew at an average rate of 2.22 percent per year. For the first 15 years of the 21st century so far, this key measure of the overall standard of living has grown, on average, at only 0.89 percent.

Of course, a growth rate per person of 0.89 percent is still growth, and growth in output per person sustained over years is still a notable achievement of the market economy.

But the difference between growth rates of something over 2 percent and a little less than 1 percent is a very big deal. How much difference does that drop make, if it continues? Thanks to the always-surprising power of compound growth rates over time, the difference in the resulting long-term standard of living is huge.

In a lifetime of 80 years, for example, per capita GDP growth of 0.89 percent per year will double the economic standard of living-on average, people will become twice as well off as before. But with a growth rate of 2.22 percent, GDP per capita will more than quintuple in the same 80 years-people will be five times as well off. Such amazing improvement has actually happened historically beginning with the economic revolutions of the 19th century and continuing through the 20th. In 1950, U.S. real per capita GDP was $14,886 (using constant 2009 dollars). By 2000, it was $44, 721-thus 3X in 50 years.

The downshift of our new century is apparent when we look at the average growth rates in successive 15-year periods, as shown in the table.

Why the downshift and will it continue? The answer, as with so many things in economics, is that we do not know.

One theory now proposed is “secular stagnation.” This is not really so much a theory as giving a different name to slower growth rates. “Stagnation” was also a noted economic assertion in the 1940s– just before the postwar boom and on the verge of 50 years of solid growth. The great economist, Joseph Schumpeter, writing in 1949 on “modern stagnationism,” observed that “stagnationist moods had been voiced, at intervals, by many economists before.” Now they are being voiced again. They were always wrong before. Will they be right this time?

Among the factors we may speculate contribute to the markedly slower growth in real per capita GDP of this century are: the drag from financial crises and their resource misallocations; the aging of the population, with lower birth rates and long retirements; the fall in labor participation rates, so there are fewer producers as a percent of the population; the ever-more oppressive tangle of government regulations, so that “compliance” with the orders issued by bureaucrats becomes the top priority; and the massive monetary distortions of central banks, pretending to know what they are doing.

Can all this continue to suppress the underlying growth dynamic of scientific advance, innovation, entrepreneurship and enterprise of a market economy? Unless the government interventions get a lot worse (which they may!), I believe the current stagnationists will likely join their historical predecessors among the ranks of the false prophets. Let us hope so.