Tags

Financial Systemic Issues: Booms and Busts - Central Banking and Money - Corporate Governance - Cryptocurrencies - Government and Bureaucracy - Inflation - Long-term Economics - Risk and Uncertainty - Retirement Finance

Financial Markets: Banking - Banking Politics - Housing Finance - Municipal Finance - Sovereign Debt - Student Loans

Categories

Blogs - Books - Op-eds - Letters to the editor - Policy papers and research - Testimony to Congress - Podcasts - Event videos - Media quotes - Poetry

We won’t know the final lessons of QE until it’s over

Published in Real Clear Markets.

A justly famous line of John Maynard Keynes is: “Soon or late, it is ideas…which are dangerous for good or evil.”

The first lesson from ten years of Quantitative Easing (QE) is that the ideas of those who run fiat currency central banks, as these ideas change over time and go in and out of central bank fashion, are extremely important for good or evil, on a very large scale.

Contrasting the ideas of QE to earlier governing ideas of the Federal Reserve is instructive. In the 1950s under Chairman William McChesney Martin, the Fed adopted the “bills only” policy. That meant the only investment assets from the Fed’s open-market operations were short-term Treasury bills. The theory was that the Fed’s open market interventions should not operate directly on long-term interest rates and should never try to allocate credit among economic sectors.

This was clearly the opposite of the theory of QE. It was not a policy directed at financial crisis, as QE originally was. But the last crisis has now been over for a long time, and QE still amounts to $4.2 trillion on the balance sheet of the Fed.

How many Treasury bills does the Fed own today? The answer is zero.

So over 50 years, the Fed has gone from believing in all Treasury bills to no Treasury bills.

Another lesson of QE: Do not look for the ideas of central bankers to be eternal verities—they aren’t. The times call forth the ideas, for better or for worse.

The Credit Crunch of 1966 was created by the Fed’s regulatory ceilings for interest rates—the Fed used to believe in those, too. In that year, mortgage lending funds dried up, the savings and loan industry (then politically powerful, believe it or not) was unhappy, and many in Congress wanted the Fed to buy the bonds of Fannie Mae and the Federal Home Loan Banks in order to support housing and housing finance.

Chairman Martin did not agree. Correctly pointing out that this would be credit allocation by the Fed, he found it a bad idea “to divert open market operations from general economic objectives to the support of specific markets for credit.” This would “violate a fundamental principle of sound monetary policy, in that it would attempt to use the credit creating powers of the central bank to subsidize programs benefitting special sectors of the economy.”

In my judgment, Martin was right about this, but Congress loves nothing better than to subsidize and overleverage real estate. Here was the consequent threatening message to the Fed sent by a future Banking Committee chairman, Senator Proxmire, in a 1968 hearing:

“You recognize, I take it, that the Federal Reserve Board is a creature of Congress?

The Congress can create it, abolish it, and so forth?

What would Congress have to do to indicate that it wishes the Board to change its policy and give greater support to the housing market?”

If Proxmire were still alive, he would presumably be a fan of QE forever.

The new Fed Chairman, Arthur Burns, who arrived in 1970, decided that the Fed should “demonstrate a more cooperative attitude.” So by the 1980s, the Fed’s bond portfolio came to include the debt of Fannie Mae, the Federal Home Loan Banks, the Farm Credit Banks, the Federal Land Banks, the Federal Intermediate Credit Banks, the Banks for Cooperatives, the United States Postal Service, Ginnie Mae, the General Services Administration, the Farmers Home Administration, the Export-Import Bank, and even the Washington Metropolitan Area Transit Authority. In other words, the Fed was helping fund the Washington DC Metro system! That was along with funding Fannie Mae when it was insolvent on a mark-to-market basis, as well as the Farm Credit System when it was broke.

Still, at their peak, all these totaled about $9 billion—or about 0.2% of the current size of QE.

Let’s review where the Fed’s QE-dominated balance sheet is now. As of May 30, 2018, it includes:

Treasury bills: zero

Longer term Treasury securities: $2.4 trillion

Long-term mortgage-backed securities: $1.8 trillion.

These MBS are funded with floating-rate deposits, which makes the Fed in effect the biggest savings and loan in the world. Even if we needed the world’s biggest S&L in the crisis—do we now?

Total assets: $4.3 trillion

Total capital: $39 billion

This means the Fed is leveraged 110 to 1.

As we know, the immense QE portfolios are very slowly running off—not being sold. Among the reasons for not selling is that the Fed does not want to face the very large losses in its super-leveraged balance sheet that it would probably realize when selling any meaningful part of its huge, unhedged QE position.

Another lesson: It is easier for a central bank to get into a QE portfolio than to get out.

Thus, the exit strategy is constrained to being very gradual, accompanied by the Fed’s intense hope that the ultimate adjustment in inflated house prices, and inflated stock and bond prices, will also be gradual. This is especially true for house prices, which affect 64% of American households.

Here is a further QE lesson, this one fundamental: In principle, a fiat currency central bank can make unlimited investments in anything, financed by monetization.

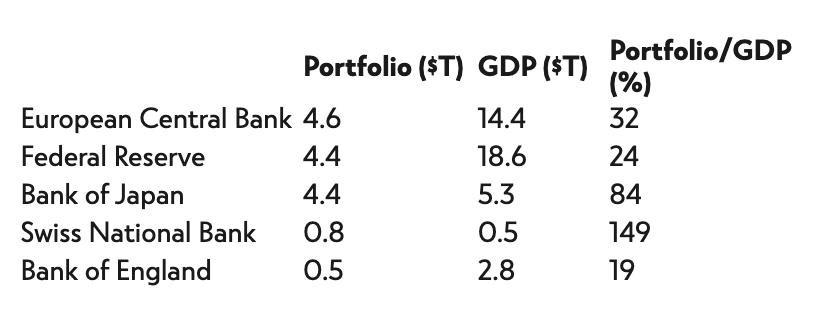

The Federal Reserve is the champion investor in mortgages. The European Central Bank has invested in corporate bonds, government agencies, regional and local government debt, asset-backed securities, and covered bonds (which include mortgages). The Bank of Japan has bought asset-backed securities and equities, in addition to vast amounts of government debt. The Swiss central bank has a huge portfolio of foreign currency bonds, a big position in U.S. equities, and also makes loans to domestic mortgage companies.

The Swiss central bank, by the way, is required by law to mark its investment securities to market, a discipline the Fed sedulously avoids.

All of these versions of QE involve credit allocation. In the case of the Fed, its two favored allocations are housing and long-term financing of the government deficit.

The only limits to what a fiat currency central bank can finance and subsidize are: the law, politics, and the ideas of central bankers. There are no intrinsic financial constraints.

Whether there will be new legal and political constraints in the future depends, I believe, on how the end of the QE experiments ultimately turn out. In other words, will the correction of the QE-induced asset price inflations be a soft landing or a hard landing? If the latter, you can easily imagine a legislature wanting to enact future constraints.

Ten years into QE, what should the Fed be doing now? The distinguished expert on central banking, Charles Goodhart, recently wrote that it is “generally agreed” that “Where the QE involved directional elements, to support credit flows through critical but weak markets, e.g. the mortgage market in the USA, such assets should be entirely run off, and the assets left in the central bank’s balance sheet should be entirely in the form of government debt.”

With all due respect to Senator Proxmire, this seems correct to me.

But, as Goodhart continues, it does not answer a further question QE makes us ask: What is the optimal size of central bank balance sheets in normal times? They have become so large—how much smaller should they get?

Other related questions include: Will the central banks’ credit allocations become viewed in retrospect as misallocations? And how should we understand the respective roles of the Treasury and the central bank? Are they essentially one thing masquerading as two, as QE tends to suggest?

I conclude with a final lesson: We won’t know what the final lessons are until after the exit from QE has been completed. It ain’t over till it’s over.

The great waves of industrial innovation

Published in Law & Liberty.

How did the world of lord and serf, horse and carriage, superstition and disease, turn into the world of boss and worker, steam and steel, science and medicine?

Jonathan Steinberg asks us to ponder this in his lecture series “European History and European Lives: 1715 to 1914.” We can add to his question, among countless other things previously unimaginable, “and the world of jets and space probes, computers and Google searches, antibiotics and automatic washing machines, and sustained long-term economic growth per capita?” Relative to all previous human life, this new world, the one we live in, is truly astonishing. As Steinberg asks us to wonder, “How and why did what we call the modern world come about?”

The answer at the most fundamental level is through the creation and harnessing of scientific knowledge. Far and away the most important event in all of history was the invention of science based on mathematics by the geniuses of the seventeenth century. This is symbolized above all by Isaac Newton, whose masterwork, Philosophiae Naturalis Principia Mathematica, we may freely render into English as “Understanding Nature on Mathematical Principles.” The invention of mathematicized science was the sine qua non of the modern world. Other important modernizing developments in government, law and philosophy are handmaidens to it.

As Alexander Pope versified the impact:

Nature and Nature’s laws lay hid in night:

God said, Let Newton be! And all was light.

Of course, the translation to the modern world was not quite that direct. The new and multiplying scientific knowledge had to be transferred into technical inventions, those into economically useful innovations, those expanded into business ventures by entrepreneurial enterprise, and with the development of management processes for large-scale organizations, those spread around the world in great waves of industrial innovation.

We may picture these great waves over the last two and a half centuries like this:

Waves of Innovation

The result of these sweeping creations by the advantaged heirs of the Newtonian age is the amazing improvement in the quality of life of ordinary people like you and me. As measured by real GDP per capita, average Americans are about eight times better off than their ancestors of 100 years ago. (They in turn were far better off than their predecessors of the 18th century, when the modern world began to emerge.)

In 1897, average industrial wages per week have been estimated at $8.88. That was for a work week of about 60 hours (say six ten-hour days—and housewives had to work 70 hours a week to keep home life going). The industrial wages translate to 15 cents an hour. Correcting for inflation takes a factor of about 25, so 15 cents then is equivalent to $3.75 today. Current U.S. average hourly manufacturing wages are $21.49, adding benefits gives total hourly pay of over $30. In other words, real industrial hourly pay has multiplied about eight times. While this was happening, over the course of a century a lifetime’s average working time per day fell in half, while average leisure time tripled, according to estimates by Robert Fogel.

Along the way, of course, there were economic cycles, wars, recessions, depressions, revolutions, turmoil, crises, banking panics, muddling through and making mistakes. But the great waves of industrial innovation continued, and so did the improving standard of living on the trend.

Joseph Schumpeter memorably summarized the point of economic growth as not consisting in “providing more silk stockings for queens, but in bringing them within the reach of factory girls in return for steadily decreasing amounts of effort.” The Federal Reserve Bank of Dallas demonstrated how more goods for less effort indeed happened—showing how prices measured in hours and minutes of work at average pay dropped dramatically during the twentieth century. Their study, “Time Well Spent—The Declining Real Cost of Living in America,” is full of interesting details—here are a few notable examples. The time required to earn the price of milk fell 82%; of a market basket of food, 83%; of home electricity, 99%; of a dishwashing machine, 94%; of a new car, 71%; and of coast-to-coast airfare, 96%. Of course, no amount of work in the early twentieth century could have bought you an iPhone, a penicillin shot, a microwave oven, a ride on a jet across the Atlantic Ocean, or a myriad of other innovations.

These advances in the economic well-being of ordinary people are consistent with a famous prediction made by John Maynard Keynes in 1930. In the midst of the great global depression, which might have led to despair about the future, Keynes instead prognosticated that the people of 2030, of 100 years from then, would be on average four to eight times better off due to innovation and economic growth. As 2030 approaches, we can see that his forecast will be triumphantly fulfilled near the top of its range.

How much can the standard of living continue to improve? In 1900, according to Stanley Lebergott, the proportion of Americans who had flush toilets was only 15%. Only 24% had running water, 1% had central heating, 3% had electricity, and 1% owned an automobile. The people of that time could not imagine ordinary life as it is now. Correspondingly, it is exceptionally difficult for us to imagine how hard, risky and toilsome the average life was then.

And if we try to imagine the ordinary life of 100 years into the future, can we think that people will once again be eight times better off than we are? Can the great waves of innovation continue? Julian Simon maintained that since human minds and knowledge constitute “the ultimate resource,” they can. “The past two hundred years brought a great deal of new knowledge relative to all the centuries before that time,” he wrote, “the past one hundred years or even fifty years brought forth more than the preceding one hundred years,” and we can confidently expect the future to continue to “bring forth knowledge that will greatly enhance human life.”

S. 2155 won’t end finreg debate, but it’s an important first step

Published in Real Clear Markets.

S. 2155 won’t end finreg debate, but it’s an important first step

The U.S. House reportedly will move next week to take up and pass a modest financial regulatory reform bill already approved by the Senate – S. 2155, the Economic Growth, Regulatory Relief and Consumer Protection Act.

This is not the fundamental reform of the bureaucracy-loving Dodd-Frank Act of 2010 one might once have hoped for, nor is it the much broader reforms proposed by the House Financial Services Committee in its Financial CHOICE Act. But everyone agrees the current political reality is that the latter bill cannot be enacted, while the current bill is a step forward that can actually be taken. A modest step forward is better than standing still.

Small banks and credit unions, defined in the bill as those with assets of less than $10 billion, will be the principal beneficiaries of its reforms, by reducing their compliance burdens with onerous regulations that were inspired by the political emotions of 2010 in the wake of the financial crisis. These lenders are less than 0.5 percent the size of JPMorgan Chase. The costs and burdens of complex and opaque regulation are disproportionately heavy for them.

Community banks and credit unions are enthusiastic supporters of the bill and its expected enactment will be an important victory for them. Small banks represent the vast majority of all banks. There are 5,670 federally insured depository institutions in the United States. Of these, 5,547 or 98 percent, have assets of less than $10 billion. On a still smaller scale, 4,920, or 87 percent of all banks, have assets of less than $1 billion, which makes them less than 0.05 percent the size of JPMorgan.

Among other regulatory de-complexification, the bill would provide small banks the option to have a high and simple leverage capital requirement (tangible equity as a percentage of total assets) replace the complicated risk-based capital calculations arising from the international negotiations known as the “Basel” rules (named after the city in Switzerland). It provides for this ratio to be set in a range of 8 percent to 10 percent. The similar idea of the CHOICE Act specified 10 percent. If combined with a simple liquidity requirement, this is an excellent idea.

A key improvement in the bill is that, for small banks, residential mortgage loans they make and keep for their own portfolio would be considered “qualified mortgages” for compliance with the Dodd-Frank Act. This recognition is essential; when a bank keeps the mortgage loan and all its risks, putting up its own capital as “skin in the game,” it is in a different financial world from those who make the loan and forthwith sell it, passing all the risk to somebody else. Much of the regulatory motivation of the Dodd-Frank Act was trying to deal with the moral hazard of the “originate and sell” mortgage model. That the “skin in the game” model is fundamentally different should have been obvious all along, but better late than never. A sad irony is that the “originate and sell model,” with the flaws that later became so evident, was strongly pushed by government policy, subsidies and regulation.

This regulatory reform bill is pretty complex. In draft form, it is 192 pages long, with many provisions devoted to particular constituency concerns, as you might expect from something that needed a bipartisan deal to get through the Senate. You might say it displays Madisonian balancing of competing concerns of interest groups (or as Madison would have put it, “factions”). Everybody cannot like everything in it.

A sampling of its various provisions includes:

For big banks, increasing the level at which they are automatically considered “systemically important” from $50 billion to $250 billion in assets—subject to regulators’ ability to overrule in particular cases.

A special deal on the leverage capital requirement for banks whose principal business is custody of assets (there are only a couple of them).

More favorable treatment of investment grade municipal bonds for purposes of big bank liquidity requirements. In addition to helping big banks, this is naturally very popular with issuers of municipal securities.

A regulatory simplification for closed-end mutual funds.

A break on the treatment of certain brokered deposits, useful to some small banks.

Easier treatment of some riskier commercial real estate loans. This is popular with real estate developers, of course. Since commercial real estate is often at the center of banking busts, this may be the most dubious of all the bill’s provisions.

A choice for federal savings associations to have regulatory treatment just like national banks. This is a natural step in the gradual disappearance of a separate savings and loan industry. It is now hard to remember that a special savings and loan industry was in former days considered an important national financial priority.

Not to be forgotten is an additional taking of the Federal Reserve Banks’ retained earnings, to help reduce the budget deficit.

And numerous other special provisions, displaying that the bill is indeed a product of a democratic legislative processes.

Taking the bill all in all, it should be enacted. But it should by no means be the end of regulatory reform. The House has a lot of ideas for additional steps, many with bipartisan support. We’ll see if anything else happens.

How does our ‘Great Recession’ compare to ones from the past?

Published in Real Clear Markets.

A prominent economist opened his book, The Great Recession, with this observation: “In the years ______, the world economy passed through its most dangerous adventure since the 1930s.” This should sound familiar. “Its world-wide character and the associated bankruptcies and financial disturbances,” he added, “made this episode the long-awaited postwar economic crisis.” But what years was Otto Eckstein in fact describing, so how do you fill in the blank in the first quotation? The correct answer is the great recession of 1973-75. (How did you do on the quiz, esteemed Reader?)

“The capitalist process progressively raises the standard of life for the masses,” wrote the ever-provocative Joseph Schumpeter, but “It does so though a series of vicissitudes.” Further, “Economic progress, in capitalist society, means turmoil.” If Schumpeter is right that progressively raising the standard of living for ordinary people requires vicissitudes and turmoil, then cycles of booms and busts do not just happen, but are necessary in theory to economic progress. They certainly do seem unavoidable so far. Empirically, recessions are reasonably frequent. In the last 100 years, there were 18 recessions in the United States, thus on average about once every 5 1/2 years. In the last 50 years, there have been seven recessions or on average once about every seven years.

Many recessions are shallower, but there are occasional great recessions. How does “our” great recession—that of 2007-09– look relative to some of its predecessors? Specifically, we compare it to the great recessions of 1981-82, 1973-75, and 1937-38.

The 2007-09 great recession led to a U.S. unemployment rate peak of 10.6%. This was surely bad, but not as bad as the 11.4% which followed the 1981-82 bust. The unemployment rate in 1973-75 got to 9.1%. The great recession of 1937-38 was far worse, with unemployment peaking at about 20%. (These unemployment rates are not seasonally adjusted.)

For 2007-09, 477 financial institutions failed in the five years from the onset of the great recession. For 1981-82, the comparable number is 625 financial institution failures. In the five years after 1973, there were 46 failures, but it is possible that the whole banking system was insolvent on a mark-to-market basis. There were 262 failures in the five years after 1937.

In terms of peak-to-trough drop in real GDP, 2007-09 is the second worst of our examples. In order of increasing severity the aggregate real GDP changes were: 1981-82, -2.8%; 1973-75, -3.1%; 2007-09, -4.2%; and estimated for 1937-38, -18%.

These great recessions had very different inflation experiences. In 1973-75, in addition to the high unemployment, the U.S. suffered from painful double-digit inflation rates, with an annualized average of 10.9% on top of the other problems. In 1981-82, the inflation rate was 5.2% along with recession, compared to 1.8% in 2007-09. In 1937-38, they had deflation, or an inflation rate of -1.9%.

Then there is the cratering of the stock market in each case. As measured by the peak to trough percentage drop in the Dow Jones Industrial Average, “our” great recession was the worst, with a 52% drop. In 1937-38, the drop was 48%. The DJIA fell 39% in 1973-75, and 20% 1981-82. All painful, to be sure, especially if you were on margin.

Short-term interest rates fell dramatically in all four great recessions, but from very different levels. Three-month Treasury bill yields started the 1981-82 great recession at the remarkable level of 15% and fell to 8.1%, the biggest change in number of percentage points. The biggest drop measured as a percentage of the initial level was our 2007-09, in which three-month bill yields dropped from 3% to 0.18% or by 94%. In 1973-75, these yields went from 7.8% to 5.5%, which sounds still very high to us now. The lowest trough in rates was in 1937-38, when three-month bills went down to 0.05% from 0.41%.

In sum, the great recession of 2007-09 has predecessor great recessions. These were worse in some ways, less bad in other ways, and present different combinations of painful problems. All were severe downers. But great recessions and ordinary recessions notwithstanding, on the trend the enterprising economy keeps taking income per capita ever higher, “progressively raising the standard of life for the masses” over time. If there is some way to do that without the cycles, it has yet to be discovered.

What you would have made if you bought big lenders in 2006

Published in Real Clear Markets.

Lending money is a risky business. Lending money when the lender is itself highly leveraged is more risky yet. How bad can the result of this simple fact be for investors in common stock? And have such investors yet recovered from the crisis of 2007-2009?

Suppose you had decided at the end of 2006, when it looked like lending businesses were booming, to invest $10,000 equally divided among the common stock of the dozen biggest U.S. lending institutions. Those would have been eight bank holding companies, two thrift holding companies and two government-sponsored enterprises. Specifically, ranked by total assets, that would have been: Citigroup, Bank of America, JPMorgan, Fannie Mae, Freddie Mac, Wachovia, Wells Fargo, Washington Mutual, U.S. Bancorp, Countrywide Financial, SunTrust and National City.

How would you have done? Your portfolio, bought for $10,000, would at the end of March 2018, eleven years later, been worth $5,960. You would be still be down more than 40 percent. Of course, you are now better off than at the bottom of the stock market in 2009, when it was worth $2,569, or down 74 percent. But the more than eight years since have not gotten you back to even, far from it. The unfortunate history of your big lender portfolio is shown in the following table.

S&P Global Intelligence

You are also in poor shape relative to the Standard & Poor’s 500 index. As of March 2018, you are about 68 percent behind the alternative of having put your $10,000 in the S&P. Your current $5,960 compares to the index’s current $18,620. The history of the relationship is shown in the following graph.

S&P Global

Of course, the performance over the whole period of the lenders’ individual stocks varies by a lot. From the virtually 100 percent loss in Washington Mutual, to the 98 percent losses in Fannie and Freddie, to the 88 percent loss in Citigroup and 44 percent loss in Bank of America, we find gains of 47 percent in Wells Fargo and 128 percent in JPMorgan. Overall, there are nine institutions with their value still down after more than 11 years and only three that are up versus 2006.

It is true that financial markets are always energetically looking forward with thousands of eyes, minds and computers. But despite the diligent efforts, they often don’t see forward very well. So indeed it was in 2006, with the stock prices of the biggest lending institutions at the top of the first (and assuredly not the last) great 21st century bubble.

Slick accounting at the Federal Reserve could prove disastrous

Published in The Hill.

“Mr. Chairman, on exhibit two, panel four, ‘deferred asset.’ This is kind of a nice term, ‘deferred asset.’ As far as I know, the committee has never used the deferred asset. It strikes me as a possible political firefight to bring that into play. All of the scenarios here, other than option one, if I’m reading this correctly, would bring the deferred asset into play, with possible repercussions, I think, for the Federal Reserve.”

This was James Bullard, president of the Federal Reserve Bank of St. Louis, speaking at the September 2012 meeting of the Federal Open Market Committee, according to the minutes. Said a staff member in reply, “It has never been the case that we have had, for the Federal Reserve System as a whole, a deferred asset.” But they knew that they might have one going forward. Earlier in the meeting, the staff had reported that all the options considered to reduce the Fed’s bond portfolio would cause the “creation of a deferred asset,” perhaps even a “substantial deferred asset.”

What in the world were they talking about? In this context, what did this, as Bullard ironically said, “nice” term mean? In fact, they were discussing how, if they ever tried to reduce their huge portfolio of long-term Treasuries and mortgage-backed securities, they were liable to take big losses. They were pondering the effect which the losses arising from any attempt to normalize their balance sheet would have on their financial condition.

What the Fed meant by “deferred asset” in clear language is the “net losses we would take.” What would be deferred is the recognition of the losses in retained earnings. The losses under consideration might occur by selling some of the Fed’s vast investment in long-term securities for less than it paid for them. Could this happen? Of course. Buy at the top for $100 and sell later for $95 means a loss of $5 for anybody.

Already in 2012, the Federal Open Market Committee was struggling with the clear possibility that such losses could be very large, indeed much larger than the Fed’s net worth. Thus, such losses had the potential to render the central bank insolvent on a balance sheet basis, as well as making it it so that the Fed would be sending no money to the Treasury to reduce the budget deficit, perhaps for several years.

In one scenario presented to the Federal Open Market Committee at that 2012 meeting, the “deferred asset” would get to about $175 billion. At the time of the meeting, the Fed’s net worth was only $55 billion, so its leaders were contemplating the possibility of losing up to three times its capital. This was happening while running a long-term securities portfolio of $2.6 trillion.

If negative net worth did arrive, the Fed could still print any money needed to pay its bills, but the balance sheet wouldn’t look so good. And might not publishing a balance sheet with negative net worth mean a “possible political firefight” in Bullard’s phrase? What might Congress say or do? The Fed didn’t want to find out. So it invented having a “deferred asset,” if necessary, rather than reporting a negative net worth.

In short, this “deferred asset” would be an imaginary asset. It would be booked in this fashion to avoid recognizing the effect of net losses on capital. In accounting terms, it would be a big debit looking for someplace to go. The proper destination of the debit for everybody in the world, including the Fed, is to retained earnings, where it would reduce capital, or even make it negative. But the Fed does not choose to allow this, and the central bank defines its own accounting rules.

So the Fed would send the debit to an accounting “deferred asset” instead, which hides the loss and overstates capital. Harshly described, for ordinary banks, this would be called accounting fraud. So more than five years ago, the Fed understood very well the big losses that might result from its massive “quantitative easing” investments, and how such losses might dwarf the Fed’s capital. It knew it could prevent showing a negative net worth by a slick accounting move. Hence the extensive discussion of the “deferred asset,” which does indeed sound a lot better in the minutes than “negative capital.”

Since then, the Fed’s portfolio is much bigger, up to $4.2 trillion, so the potential losses are much bigger now, while the Fed’s capital is much smaller, down to $39 billion because the Congress expropriated a lot of its retained earnings. Interest rates have gone up. Selling down the Fed’s portfolio could now cause an even bigger negative net worth, or “deferred asset.” As we know, the Fed has concluded not to make any sales, only move extremely slowly toward balance sheet normalization by holding all its long-term portfolio to maturity.

Should the Federal Reserve, in the circumstances of 2012 or now, reveal the projected losses from any portfolio sales and resulting “deferred asset” to the public? Should it discuss candidly with its boss, the Congress, how big the losses and negative net worth might turn out to be? Or should it just prepare the accounting gimmick for use, if necessary, worry in private, put on a good face in public, and hope for the best? What would you do, thoughtful reader, in their place?

Federal Reserve will be judged by future on these years of low rates

Published in The Hill.

The government’s official interest rate price-fixing committee, otherwise known as the Federal Reserve, has just raised its target fed funds rate by a quarter-point. This surprised no one, as the Fed intended, since it works hard to manage expectations.

What would the rate be if it were set in private markets instead of by a government committee? No one knows, but presumably it would be higher.

The Fed’s latest move still leaves interest rates at remarkably low levels. In the 1980s and 1990s, most people would have considered it impossible for the fed funds rate to be under 2 percent. Now we have the Fed’s current target range of 1.5 to 1.75 percent—to make it easy, let’s just call it 1.75 percent. Not only is this rate low, but in real inflation-adjusted terms, it is negative. In February, the Consumer Price Index went up 2.2 percent year-over-year, so the new fed funds target in real terms is 1.75 percent minus 2.2 percent = negative 0.45 percent.

It looks like it will take one more increase, at least, to get the real fed funds rate up to around zero and numerous increases after that to approach a normal level. Needless to say, normal real interest rates are positive, not negative.

What might a normal level be? We can make a fair guess by looking at long-term averages. Graph 1 shows nominal fed funds rates and inflation rates from mid-1954 to year-end 2017.

Over this long term, the fed funds rate averaged 4.86 percent. The annual rate of inflation averaged 3.56 percent. So the long-term average real fed funds rate was 1.3 percent.

If inflation going forward runs at the Fed’s target inflation rate of 2 percent, it would suggest a normalized fed funds rate of 3.3 percent. To get there would take six more quarter-point increases. On similar logic, the normalized yield on the 10-year Treasury note would be 4.5 percent, instead of the current 2.8 percent, and the rate on a 30-year mortgage loan would be 6.2 percent, up from the current 4.4 percent level. Of course, if inflation turns out to move higher than 2 percent, the normalized fed funds rate, and also the other rates, will be correspondingly higher.

Graph 2 shows the real fed funds rates over the same years.

As is apparent from this graph, we have lived through and remain in an exceptionally long period of negative real fed funds rates. It is by far the longest stretch of such negative real rates in our six decades of data. While normal real fed funds rates are positive, it is not unusual for them to be negative for some periods, such as when the Fed is facing a recession, or a financial crisis, or both, or has a desire to inflate asset prices. Extended negative real interest rates are good at inducing asset-price booms.

Since the 1950s, there were negative real fed funds rates during the following times:

Six quarters during 1956-1958;

Two quarters during 1970-1971;

15 quarters during 1974-1977;

Five quarters during 1979-1980;

Three quarters at about zero in 1992-1993;

11 quarters during 2002-2005;

Three quarters in 2008.

And then the all-time champion run of negative real fed funds rates:

30 quarters, equivalent to 7.5 years, during 2009 to now.

It is hardly surprising that this period has been accompanied by booms in equity, bond and house prices. Was the Fed’s strategy during these years wise? The future will judge that, looking back.

For now, we can say, in sum, that the Fed’s target fed funds rate remains remarkably low, is still negative in real terms, and has a long way to go to get back to normal.

Economic crises are invariably failures of the imagination

Published in Real Clear Markets.

A fundamental issue in all risk management is oversight vs. seeing. You can be doing plenty of oversight, analysis, regulation and compliance, with much diligence and having checkers check on checkers, but is the whole process able to envision the deep and surprising risks that are the true fault lines under your feet? Or are you only analyzing, regulating, writing up and color coding dozens of factors which while important, are not the big risk which is going to take you and perhaps the system of which you are a part, down? For example, in the midst of your risk management oversight efforts, whether as a company or as the government, could you see in 2005 or 2006, or at the latest by 2007, that U.S. average house prices across the whole country, were likely to drop like a stone? And see what would happen then?

Most people, including the most intelligent, experienced and informed, could not.

Former Treasury Secretary Timothy Geithner, in his memoir of the 2007-2009 financial crisis, Stress Test (2014), draws this essential conclusion: “Our crisis, after all, was largely a failure of imagination. Every crisis is.” If you can’t imagine it, if you consider that the deep risk event is unimaginable or impossible, your oversight will not see the risk. “For all our concern about ‘froth’,” Geithner continues, “we didn’t foresee how a nationwide decline in home prices could induce panic in the financial system.”

This is a profoundly important insight. Geithner expands on it: “Our failures of foresight were primarily failures of imagination, like the failure to foresee terrorists flying planes into buildings before September 11. But severe financial crises had happened for centuries in multiple countries, in many shapes and forms, always with pretty bad outcomes. For all my talk about tail risk, negative extremes, and stress scenarios, our visions of darkness still weren’t dark enough.”

That was not for lack of effort, but for lack of seeing. “The actual main failing was over-reliance on formal econometric models,” banking scholar Charles Goodhart suggests in his acute essay, “Central bank evolution: lessons learnt from the sub-prime crisis” (2016). He points out that as the housing bubble was inflating, there was copious housing finance data which could be and was analyzed:

“There were excellent monthly data on virtually all aspects of mortgage finance in the USA starting from the 1950s. By the 2000s such data provided over 50 years of all aspects of US mortgage finance. During this period, there had only been a very few months in which the value of houses, and the mortgages related to them, of a regionally diversified portfolio of housing assets over the US as a whole had faced a loss, and then only a very small one.

“While there had been sharp declines in housing valuations in certain specific regions, i.e. the North East in 1991-2, the oil producing states in the mid-1980s, etc., a regionally diversified portfolio virtually never showed a loss, and then only a minor one, over these 50 years.” The conclusion seemed clear enough at the time: house prices did not, so would not, fall on a national average basis. A portfolio of mortgages diversified across regions would be protected. “Virtually everyone was sucked into the general conventional wisdom that housing prices”—on average—“were almost sure to continue trending generally upwards.”

This clear, though in retrospect completely wrong, conclusion could be professionally quantified: “Put those data into a regression analysis, and then what you will get out is an estimate that any loss of value in a regionally diversified portfolio of greater than about three or four percent would be…highly improbable.” But as the bubble got maximally inflated, its shriveling became highly probable instead of improbable. As we know, average U.S, house prices went down by 27% and fell not for a few months, but for six years, in spite of all kinds of government interventions. The housing market went down for longer than a great many people could stay solvent.

“Of course,” Goodhart reminds us, “econometric regressions are based on the implicit assumption that the future will be like the past.” The less of the past we know, the worse an assumption this is. In this case, fifty years and one country, even a very big country, were not enough.

To expand how much of the past we have studied, both in terms of more time and more places, is perhaps one way to improve our ability to see risks, imagine otherwise unimaginable outcomes, and thus improve our risk oversight. Perhaps. There are no guarantees of success.

House prices: What the Fed hath wrought

Published in The Hill.

After the peak of the housing bubble in 2006, U.S. house prices fell for six years, until 2012. Are these memories getting a little hazy?

The Federal Reserve, through forcing years of negative real short-term interest rates, suppressing long-term rates, and financing Fannie Mae and Freddie Mac to the tune of $1.8 trillion on its own vastly expanded balance sheet, set out to make house prices go back up. It succeeded. Indeed it has overachieved. Average house prices are now significantly higher than they were at the top of the bubble. This is shown in the following 20-year history of the familiar S&P Case-Shiller national house price index.

Read the full article here.

Banks need more skin in the housing finance game

Published by American Banker.

We all know it was a really bad idea in the last cycle to concentrate so much of the credit risk of the huge American mortgage loan market on the banks of the Potomac River — in Fannie Mae and Freddie Mac.

But the concentration is still there, a decade later.

The Fannie and Freddie-centric U.S. housing finance system removes credit risk from the original lenders, taking away their credit skin in the game. It puts the risk instead on the government and the taxpayers.

Many realized in the wake of the crisis that this was a big mistake (although a mistake made by a lot of smart people) in the basic design of the inherently risk-creating activity of lending money. Many realized after the fact that the American housing finance system needed more credit skin in the game.

Skin-in-the-game requirements were legislated for private mortgage securitizations by the Dodd-Frank Act, but do not apply to lenders putting risk into Fannie and Freddie. Regulatory pressure subsequently caused Fannie and Freddie to transfer some of their acquired credit risk to investors — but this is yet another step farther away from those who originated the risk in the first place.

That isn’t where the skin in the game is best placed. The best place, which provides the maximum alignment of incentives, and the maximum use of direct knowledge of the borrowing customer, is for the creator of the mortgage loan to retain significant credit risk. No one else is as well placed.

The single most important reform of American housing finance would be to encourage more retention of credit skin in the game by those making the original credit decision.

In this country, we unfortunately cannot achieve the excellent structure of the Danish mortgage bond system, where 100% of the credit risk is retained by the lenders, and 100 percent of the interest rate risk is passed on to the bond market. The Danish mortgage bank which makes the loan stays on the hook for the default risk and receives corresponding fee income. The loans are pooled into mortgage bonds, which convey all the interest rate and prepayment risk to bond investors. This system has been working well for over 200 years.

There are clearly many American mortgage banks which do not have the capital to keep credit skin in the game in the Danish fashion. But there are thousands of American banks, savings banks and credit unions which do have the capital and can use to it back up their credit judgments. The mix of the housing finance system could definitely be shifted in this direction.

If you are a bank, your fundamental skill and your reason for being in business is credit judgment and the managing of credit risk. Residential mortgage loans are essential to your customers and are the biggest loan market in the country (and the world). Why do you want to divest the credit risk of the loans you have made to your own customers, and pay a big fee to do so, instead of managing the credit yourself for a profit? There is no good answer to this question, unless you think your own mortgage loans are of poor credit quality. For any bankers who may be reading this: Do you think that?

But, it will be objected: The regulators force me to sell my fixed-rate mortgage loans because of the interest rate risk, which results from funding 30-year fixed-rate loans with short-term deposits. True, but as in Denmark, the interest rate risk can be divested while credit risk is maintained. For example, the original 1970 congressional charter of Freddie provided lenders the option of selling Freddie high loan-to-value ratio loans by maintaining a 10% participation in the loan or by effectively guaranteeing them, not only by getting somebody else to insure them.

Treasury Secretary Steven Mnuchin recently told Congress that private capital must be put in front of any government guarantee of mortgages. That’s absolutely right — but whose capital? The best solution would be to include the capital of the lenders themselves.

In sharp contrast to American mortgage-backed securities in this respect are their international competitors, covered bonds. These are bonds banks can issue, collateralized by a “cover pool” of mortgage loans which remain assets of the bank. Thus covered bonds allow a long-term bond market financing, but all the credit risk stays on the bank’s balance sheet, with its capital fully at risk.

American regulators and bankers need to shake off their assumption, conditioned by years of Fannie and Freddie’s government-promoted dominance, that the “natural” state of things is for mortgage lenders to divest the credit risk of their own customers. The true natural state for banks is the opposite: to be in the business of credit risk. What could be more obvious than that?

The housing finance system should promote, not discourage, mortgage lenders staying in the credit business. Regulators, legislators, accountants and financial actors should undertake to reform regulatory, accounting and legal obstacles to the right alignment of incentives and risks. The Federal Housing Finance Agency should be pushing Fannie and Freddie to structure their deals to encourage originator retention of credit risk.

The result will be to correct, at least in part, a fundamental misalignment that the Fannie and Freddie model foisted on American housing finance.

Confiscation of gold by the federal government: A lesson

Published in Real Clear Markets.

Historically as well as now, people in America tried to protect themselves against the government’s devaluation of their dollars by holding gold; and formerly, by buying Treasury bonds which promised to pay in gold. The fundamental thought was and is the same that many holders of Bitcoin and other “cryptocurrencies” have now: hold something that the government cannot devalue the way it can its official currency.

Unfortunately for such an otherwise logical strategy, governments, even democratic governments, when pushing comes to shoving, may use force to control and even take away what you thought you had. The year 1933 and the new Franklin Roosevelt presidency provide vividly memorable, though little remembered, examples. First the U.S. Treasury defaulted on its promises to pay gold bonds in gold; then under notable executive orders, the U.S. government confiscated the gold of American citizens and threatened them with prison if they didn’t turn it in. It moreover prohibited the future holding of any gold by Americans, an outrageous prohibition which lasted four decades, until 1974.

All this may seem unimaginable to many people today, perhaps including Bitcoin enthusiasts, but in fact happened. Said Roosevelt in explanation, “The issuance and control of the medium of exchange which we call ‘money’ is a high prerogative of government.”

President Hoover had warned in 1932 that the U.S. was close to having to go off the gold standard. Running for President, Roosevelt called this “a libel on the credit of the United States.” He furthermore pronounced that “no responsible government would have sold to the country securities payable in gold if it knew that the promise—yes, the covenant—embodied in those securities was…dubious.” The next year, during Roosevelt’s own administration, this “covenant” was tossed overboard. Congress and the President “abrogated”—i.e. repudiated—the obligation of the government to pay as promised. One can argue that this was required by the desperate economic and financial times, but about the fact of the default there can be no argument.

Roosevelt’s Executive Order 6102, “Requiring Gold Coin, Gold Bullion and Gold Certificates to Be Delivered to the Government,” of April 5, 1933 marks an instructive moment in both American monetary and political history. To modern eyes, it looks autocratic, or perhaps could fairly be described as despotic.

The order begins, “By virtue of the authority vested in me by Section 5(b) of the Act of October 6, 1917,” without naming what act that is. Why not? Well, that was the Trading with the Enemy Act which was used to confiscate German property during the First World War.

The order states:

-“All persons are hereby required to deliver on or before May 1, 1933…all gold coin, gold bullion and gold certificates now owned by them or coming into their ownership.”

-“Until otherwise ordered any person becoming the owner of any gold coin, gold bullion or gold certificates shall, within three days after receipt thereof, deliver the same.”

-“The Federal Reserve Bank or member bank will pay therefore an equivalent amount of any other form of coin or currency”—in other words, we will give you some nice paper money in exchange.

Lastly, the threat:

-“Whoever willfully violates any provision of this Executive Order or of these regulations or of any rule, regulation or license issued hereunder may be fined not more than $10,000, or, if a natural person, may be imprisoned for not more than ten years, or both.”

Ten thousand 1933 dollars was a punitive fine—equivalent to about $190,000 today. But the real punishment for trying to protect your assets was “We’ll put you in jail for ten years!”

A few months later the order was revised and tightened up by Roosevelt’s Executive Order 6260, “On Hoarding and Exporting Gold” of August 28, 1933. It specifies that “no person shall hold in his possession or retain any interest, legal or equitable, in any gold,” and adds a reporting requirement: “Every person in possession of and every person owning gold…shall make under oath and file…a return to the Secretary of the Treasury containing true and complete information” about any gold holdings, “to be filed with the Collector of Internal Revenue.” So the IRS was brought in as an enforcer, too. The threat of fines and prison continued as before.

It’s a prudent idea to protect yourself against the government’s perpetual urge to depreciate its currency. But if pushing comes to shoving, how do you protect yourself against the government’s confiscating the assets you so prudently acquired—and its being willing to put you in prison if you try to keep them? What governments, even democratic ones, are willing to do when under sufficient pressure, is a lesson Bitcoin holders and everybody else can usefully consider.

Who is this ‘we’ that should manage the economy?

Published in Law & Liberty.

Adair Turner, the former Chairman of the British Financial Services Authority, has written a book about the risks and unpredictability of financial markets which has many provocative insights. It also has a frustrating blind spot about how government actions can and do contribute to financial crises.

Turner clearly addresses the failure of governments to understand what was going on as the crises of the 2000’s approached, including his notable mea culpa discussed below. But there is no discussion anywhere of the culpability of government actions which greatly contributed to inflating the bubble of housing debt and pumping up leverage on the road to the U.S. housing finance collapse.

The fateful history of Fannie Mae and Freddie Mac is not discussed, even though Turner rightly emphasizes how dangerous leveraged real estate is as a key source of financial fragility. Fannie and Freddie, with $5 trillion in real estate risk, do not rate an entry in the index.

The problems of student debt make it into a footnote in chapter six, where its rapid growth in the United States is observed, along with the judgment that “much of it will prove unpayable,” but it is not mentioned that this is another government loan program.

The role of government deposit insurance in distorting credit markets, so notable in the U.S. savings and loan collapse of the 1980s, is not considered. That instructive collapse gets one passing sentence.

The Federal Reserve, along with other central banks, created the Great Inflation of the 1970s that led to the disastrous financial crises of the 1980’s. Seeking a house price boom and a “wealth effect” in the 2000’s, the Federal Reserve promoted what turned out to be a house price bubble. Turner provides no proposals about how to control the obvious dangers of central banks, although he does point out their mistake in thinking that they had created a so-called “Great Moderation.” That turned out to have been instead a Great Overleveraging.

There can be no doubt of Turner’s high intelligence, as his double first in history and economics at Cambridge and his stellar career, leading to his becoming Lord Turner, attest. But as an old banking boss of mine memorably observed, “it is easier to be brilliant than right.”

This universal principle applies as well to leading central bankers, regulators, and government officials of all kinds as it does to private actors. The bankers “that made big mistakes,” Turner correctly says, “did not consciously seek to take risks, get paid, and get out: they honestly but wrongly believed that they were serving their shareholders’ interests.” So also for the authors of mistaken government actions: they didn’t intend to make mistakes, but wrongly believed they were serving the public interest.

When former Congressman Barney Frank, for example, the “Frank” of the bureaucracy-loving Dodd-Frank Act, said before the crisis said that he wanted to “load the dice” with Fannie and Freddie, he never intended for the dice to come up snake eyes, but they did. Throughout the book, Turner displays the tendency to assume the consequences of government action to be knowable and benign, rather than unknowable and often perverse.

Debt and the Devil opens with the remarkable confession of government ignorance shown in the following excerpts. As he became Chairman of the Financial Services Authority in 2008, Turner relates:

“I had no idea we were on the verge of disaster.”

“Nor did almost everyone in the central banks, regulators, or finance ministries, nor in financial markets or major economics departments.”

“Neither official commentators nor financial markets anticipated how deep and long lasting would be the post-crisis recession.”

“Almost nobody foresaw that interest rates in major advanced countries would stay close to zero for at least 6 [now it’s 8] years.”

“Almost no one predicted that the Eurozone would suffer a severe crisis.” (That crisis featured defaults on government debt.)

“I held no official policy role before the crisis. But if I had, I would have made the same errors.”

If governments, their regulators, and their central banks cannot understand what is happening and the real risks are, then it is easy to see why their actions may be unsuccessful and indeed generate perverse results. So we have to amend some of Turner’s conclusions, to make his partial insights more complete.

“Central banks and regulators alone cannot make the financial system and economies stable,” he says. True, but we must add: but they can make financial systems and economies unstable by monetary and credit distortions.

We are “faced with a free market bias toward real estate lending” needs additionally: and an even bigger government bias and government promotion of real estate lending.

Turner quotes Charles Kindleberger approvingly: “The central question is whether central banks can contain the instability of credit and slow speculation.” This needs a matching observation: The central question is whether central banks can hype the instability of credit and accelerate speculation. They can.

“Banking systems left to themselves are bound to create too much of the wrong sort of debt” needs amendment: Banking systems pushed by governments to expand risky loans to favored political constituencies are bound to create too much of the wrong sort of debt, which will lead to large losses. This will be cheered by the government until it is condemned.

“At the core of financial instability in advanced economies lies the interaction between the potentially limitless supply of bank credit and the highly inelastic supply of real estate.” Insightful, but incomplete. Here is the complete thought: At the core of financial instability lies the interaction between the potentially limitless supply of the punchbowl of central bank credit, bank credit, government guarantees of real estate credit, and the inelastic supply of real estate.

“Private credit creation is inherently unstable.” Here the full thought needs to be: Private and government credit creation is inherently unstable. Indeed, Turner supplies a good example of the latter: Japanese government debt has become so large relative to the Japanese economy that it “will simply not be repaid in the normal sense of the word.”

According to Turner, what is to be done? He supplies a deus ex machina: “We.” So he asserts that “We need to manage the quantity and influence the allocation of credit,” and “We must influence the allocation of credit among alternate uses,” and “We must therefore deliberately manage and constrain lending against real estate assets.” Who is this “We”? Lord Turner and his friends? There is no “We” who know how credit should be allocated.

In an overall view, Turner concludes that “All complex systems are potentially unstable,” and that is true. But it must be understood that the complex system of finance includes inside itself all the governments, central banks, regulators and politicians, as well as all the private financial actors. Everybody is inside the system; nobody is outside the system, let alone above the system, looking down with ethereal perspective and the ability to manage everything. In particular, there is no “We” outside the complex system. “We,” whoever they may be, are inside the complex system with its inherent uncertainty and instability, along with everybody else.

Time to reform Fannie and Freddie is now

Published in American Banker.

The Treasury Department and the Federal Housing Finance Agency struck a deal last week amending how Fannie Mae and Freddie Mac’s profits are sent to Treasury as dividends on their senior preferred stock.

But no one pretends this is anything other than a patch on the surface of the Fannie and Freddie problem.

The government-sponsored enterprises will now be allowed to keep $3 billion of retained earnings each, instead of having their capital go to zero, as it would have done in 2018 under the former deal. That will mean $6 billion in equity for the two combined, against $5 trillion of assets — for a capital ratio of 0.1 percent. Their capital will continue to round to zero, instead of being precisely zero.

Here we are in the tenth year since Fannie and Freddie’s creditors were bailed out by Treasury. Recall the original deal: Treasury would get dividends at a 10 percent annual rate, plus — not to be forgotten — warrants to acquire 79.9 percent of both companies’ common stock for an exercise price of one-thousandth of one cent per share. In exchange, Treasury would effectively guarantee all of Fannie and Freddie’s obligations, existing and newly issued.

The reason for the structure of the bailout deal, including limiting the warrants to 79.9 percent ownership, was so the Treasury could keep asserting that the debt of Fannie and Freddie was not officially the debt of the United States, although de facto it was, is, and will continue to be.

Of course, in 2012 the government changed the deal, turning the 10 percent preferred dividend to a payment to the Treasury of essentially all Fannie and Freddie’s net profit instead. To compare that to the original deal, one must ask when the revised payments would become equivalent to Treasury’s receiving a full 10 percent yield, plus enough cash to retire all the senior preferred stock at par.

The answer is easily determined. Take all the cash flows between Fannie and Freddie and the Treasury, and calculate the Treasury’s internal rate of return on its investment. When the IRR reaches 10 percent, Fannie and Freddie have sent in cash economically equivalent to paying the 10 percent dividend plus retiring 100 percent of the principal.

This I call the “10 Percent Moment.”

Freddie reached its 10 percent Moment in the second quarter of 2017. With the $3 billion dividend Fannie was previously planning to pay on December 31, the Treasury’s IRR on Fannie would have reached 10.06 percent.

The new Treasury-FHFA deal will postpone Fannie’s 10 percent Moment a bit, but it will come. As it approaches, Treasury should exercise its warrants and become the actual owner of the shares to which it and the taxpayers are entitled. When added to that, Fannie reaches its 10 percent Moment, then payment in full of the original bailout deal will have been achieved, economically speaking.

That will make 2018 an opportune time for fundamental reform.

Any real reform must address two essential factors. First, Fannie and Freddie are and will continue to be absolutely dependent on the de facto guarantee of their obligations by the U.S. Treasury, thus the taxpayers. They could not function even for a minute without that. The guarantee needs to be fairly paid for, as nothing is more distortive than a free government guarantee. A good way to set the necessary fee would be to mirror what the Federal Deposit Insurance Corp. would charge for deposit insurance of a huge bank with 0.1 percent capital and a 100 percent concentration in real estate risk. Treasury and Congress should ask the FDIC what this price would be.

Second, Fannie and Freddie have demonstrated their ability to put the entire financial system at risk. They are with no doubt whatsoever systemically important financial institutions. Indeed, if anyone at all is a SIFI, then it is the GSEs. If Fannie and Freddie are not SIFIs, then no one is a SIFI. They should be formally designated as such in the first quarter of 2018, by the Financial Stability Oversight Council —and that FSOC has not already so designated them is an egregious and arguably reckless failure.

When Fannie and Freddie are making a fair payment for their de facto government guarantee, have become formally designated and regulated as SIFIs, and have reached the 10 percent Moment, Treasury should agree that its senior preferred stock has been fully retired.

Then Fannie and Freddie would begin to accumulate additional retained earnings in a sound framework. Of course, 79.9 percent of those would belong to the Treasury as 79.9 percent owner of their common stock. Fannie and Freddie would still be woefully undercapitalized, but progress toward building the capital appropriate for a SIFI would begin. As capital increased, the fair price for the taxpayers’ guarantee would decrease.

The New Year provides the occasion for fundamental reform of the GSEs in a straightforward way.

FHFA’s g-fee calculation ignores the law

Published in American Banker.

In a recent report to Congress, the Federal Housing Finance Agency once again failed to satisfy a fundamental legal requirement. This is a requirement that the FHFA keeps ignoring, apparently perhaps because it doesn’t like it. But to state the obvious, the preferences of a regulatory agency do not excuse it from complying with the law.

The law requires that when the FHFA sets guarantee fees for Fannie Mae and Freddie Mac, the fees must be high enough to cover not only the risk of credit losses, but also the cost of capital that private-sector banks would have to hold against the same risk. This is explicitly not the amount of capital that Fannie and Freddie or the FHFA might think would be right for themselves, but the cost of the capital requirement for regulated private banks.

This requirement, created by the Temporary Payroll Tax Cut Continuation Act of 2011, was clear and unambiguous. The law mandated a radical new approach to setting, increasing and analyzing Fannie and Freddie’s g-fees, based on a reference to the private market. In setting “the amount of the increase,” the law said, the FHFA director should consider what will “appropriately reflect the risk of loss, as well as the cost of capital allocated to similar assets held by other fully private regulated financial institutions.”

In other words, the director of the FHFA is instructed to calculate how much capital fully private regulated financial institutions have to hold against mortgage credit risk, the required return on that capital for such private banks and therefore the cost of capital for private banks engaging in the same risk as Fannie and Freddie. This includes the credit losses from taking this risk and operating costs, both of which must be added the private cost of capital. The net sum is the level of Fannie and Freddie’s guarantee fees that the FHFA is required to establish.

The law also further requires the FHFA to report to Congress on how Fannie and Freddie’s g-fees “met the requirements” of the statute – that is, how they included the cost of capital of regulated private banks.

However, if you read the FHFA’s October 2017 report on guarantee fees, nowhere in it will you find any discussion — not a single word — about private banks’ cost of capital for mortgage credit risk. There is the same amount of discussion — zero — about how that private cost of capital enters the analysis and calculation of Fannie and Freddie’s required g-fees. Yet this is the information and annual analysis that Congress demanded of the FHFA.

Why has the agency failed to fulfill its legal obligation?

A reasonable hypothesis is that the FHFA doesn’t like the answer that results when this analysis and calculation are performed, so it is tap-dancing instead of answering the question and implementing the answer. In short, the calculation required by the law results in much a higher level of g-fees than at present. This reflects the whole point of the statutory provision — to make the private sector competitive and to take away Fannie and Freddie’s subsidized cost of capital and the distortions it creates.

The FHFA certainly understands the importance of this issue. Its report clearly sets out the components of the calculation of g-fees, saying, “Of these components, the cost of holding capital is by far the most significant.” That would be the perfect section to add the required analysis of the cost of capital for regulated private financial institutions and to use that to calculate the legally required g-fees.

But instead, the report treats us to a discussion of how “each [government-sponsored enterprise] uses a proprietary model to estimate … the amount of capital it needs.” The mortgage companies use “models to estimate the amount of capital and … [subject] that estimate to a target rate of return” to “calculate a model guarantee fee.”

That’s nice, but here are the two questions that must be answered:

What is the cost of capital for a private regulated financial institution to bear the same credit risk as Fannie and Freddie?

What is the g-fee calculation based on that cost of capital for private institutions?

The FHFA has not answered these questions. Instead, the agency said it had “found no compelling economic reason to change the overall level of fees.” How about complying with the law?

Giant ‘QE’ gamble: How will it end?

Published in the Library Of Law And Liberty.

The Federal Reserve made a colossal gamble with its so-called “Quantitative Easing” or “QE,” which is simply a euphemism for its $4.4 trillion binge of buying long-term bonds and mortgages. Its big bid for long bonds, along with parallel programs undertaken by other members of the international fraternity of central banks, has artificially suppressed long-term interest rates, and has deliberately fostered asset-price inflations in bonds, stocks and houses.

Will this gamble pan out?

The Fed now intends to reduce its buying and slowly shrink its portfolio by letting bond maturities and mortgage prepayments exceed new purchases. As its big bid is reduced, will the asset-price inflations it fostered end well in some kind of soft landing, or will they end badly in an asset-price deflation? Will the Fed be able to take its stake off the table and go away a winner—or will it ultimately lose?

Nobody knows, including the Fed itself. The officials who run the institution are guessing, like everybody else—and hoping.

In particular, they are hoping that by making the unwinding of the gamble very slow, with emphatic announcements well in advance, they will mitigate the potential negative price reactions in bond, stock and housing markets. Well, maybe this strategy will work—or maybe not. The behavior of complex financial systems is fundamentally uncertain. As Nobel laurate economist Robert Shiller said in a recent interview with Barron’s, “We don’t know what will happen in this unwinding.”

Shiller is right. But who are the “we” who don’t know? In addition to himself, “we” includes Nobel laureates, all other economists, financial market actors, regulators, the Federal Reserve, all the other central banks, and you, honored reader and me.

With its buying in the trillions, the Fed made asset prices go up and long-term interest rates go down, as intended. Simply reversing its manipulation by selling in the trillions, turning its big bid in the market into a big offer, would surely make asset prices go down and interest rates go up, perhaps by a lot. This outcome the Fed wants at all costs to avoid. So it is not selling any of its bonds or mortgages. The plan is to stop buying as much, a little at a time, while continuing the steady stream of rhetorical assurances. We don’t know, and Fed officials don’t know, if this will work as hoped.

The Fed did not strive to inflate asset prices as an end in itself, of course. The theory was that this would result in a “wealth effect,” which would in turn accelerate economic growth. Did it? Would economic growth have been worse or better without QE? Were the risks entailed in the inflation of asset prices worth whatever additional growth it may or may not have induced? In fact, U.S. real gross domestic product growth over the many years of QE has been generally unimpressive.

“Evaluating the effects of monetary policy is difficult,” as Stephen D. Williamson, an economist with the Federal Reserve Bank of St. Louis, writes in a new article in The Regional Economist, and “with unconventional monetary policy, the difficulty is magnified.” Williamson adds that “With respect to QE, there are good reasons to be skeptical that it works as advertised, and some economists have made a good case the QE is actually detrimental.” He points out that Canada without QE had better growth than the United States with it. As usual in macroeconomics, you can’t prove it one way or the other.

The Fed’s effect on asset prices seems clear, however. As one senior investment manager recently said about the price of the U.S. Treasury 10-year note, “What it tells you is the amount of distortion that quantitative easing is creating.” How much of that distortion is going to reverse itself?

With QE, the Fed has been practicing “asset transformation,” according to Williamson. That is economics-speak for borrowing short and lending long. The Fed is funding its long-term bonds and very long-term mortgage securities with short-term, floating-rate deposits. This is one of the most classic of all financial speculative gambles. In other words, the Fed has created a balance sheet for itself that looks just like a 1980s savings and loan, and has become, in effect, the biggest savings and loan in history.

Williamson reasonably asks if the Fed has any competitive advantage at holding such a speculative position, and doubts that it does. However, I believe the Fed does have two unique advantages in this respect: control of its own accounting, and lack of penalties for insolvency. The Fed uniquely sets its own accounting standards for itself, and Fed officials have decided never to mark its securities portfolio to market. More remarkably, even if it should realize losses on the actual sale of securities, officials have decided not to let such losses reduce its reported capital, but to carry the required debits to a hokey intangible asset account. No one else would be allowed to get away with that.

Suppose hypothetically that realized losses on the Fed’s giant portfolio come to exceed its small capital (less than 1 percent of the portfolio). Even then, it is not clear whether that would affect the Fed. Many economists argue that insolvency doesn’t matter if you can print the money to pay your obligations. Nonetheless, it would be embarrassing to the Fed to be technically insolvent, and its QE-unwind program is designed to avoid any realized losses while not disclosing any mark-to-market losses.

Although the GDP growth effects of the QE gamble are uncertain, it certainly has succeeded in two other ways besides inducing asset-price inflation: in robbing savers, and in allocating credit. By forcing real interest rates on conservative savings to be negative, the Fed has transferred billions of dollars of wealth from savers to borrowers—especially to the government, the biggest borrower of all, and to leveraged speculators. It has meanwhile assured the aggrieved savers that they are really better off being sacrificed for the greater good.

QE also means the Fed allocated trillions in credit to its favored sectors: housing and the government. In housing, this resulted in national average house prices inflating back up to their bubble levels, obviously making them less affordable. For the government, the Fed made financing its deficits cheaper and easier, and demonstrated once again that the real first mandate of any central bank is financing, as needed, the government of which it is a part.

As the Fed moves to unwind its big QE gamble, what will happen? It, and we, will find out by experience.

Taxpayers shouldn’t be asked to pay for Fannie and Freddie’s risk exposure

Published in The Hill.

As the old Washington saying goes, “When all is said and done, more is said than done.” This certainly applies to the years of congressional debates about how to reform Fannie Mae and Freddie Mac. They are dominant forces in the huge American mortgage market, operating effectively as arms of the U.S. Treasury.

Can you ever protect the taxpayers against the risk of Fannie and Freddie? In their current form, with virtually zero capital — and soon literally zero capital — they are and will continue to be utterly dependent on the taxpayers’ credit card for their entire existence. Every penny of their income depends on the credit support of the taxpayers.

Since 2008, Fannie and Freddie have been a $5 trillion risk turkey, roosting in the dome of the Capitol. The members of Congress are unhappy and greatly irritated by its presence, but didn’t know how to get rid of this embarrassment their predecessors created.

Of course, even before their humiliating government conservatorship, Fannie and Freddie traded every minute on the credit of the U.S. Treasury and were always were a risk to the taxpayers. Although in those days they had some positive capital of their own, it was not very much capital relative to their risks. Without their free use of the taxpayers’ credit card, they would have been much smaller, much less leveraged, much less profitable and much less risky.

Once the Congress had set up Fannie and Freddie as government-sponsored risk takers, was there any way to remove the taxpayers’ risk exposure? The historical record offers little hope. No matter what any Treasury secretary or any other politician says, or even what any legislation provides, the global debt markets will simply not believe that two institutions representing half of all U.S. mortgage credit and sponsored by the U.S. government will not be bailed out by the Treasury. And the debt markets will be right.

In 1992, while revising the legislation that governs Fannie and Freddie, Congress solemnly tried to wiggle out of the problem. It added to the statutes of the United States a provision entitled, “Protection of Taxpayers Against Liability” for Fannie and Freddie’s debts. This “protection” is still on the books, although it did not provide any protection to the taxpayers.

Title XIII, “Government-Sponsored Enterprises,” of the Housing and Community Development Act of 1992, Section 1304, pronounced:

This title may not be construed as obligating the Federal Government, either directly or indirectly, to provide any funds to the Federal Home Loan Mortgage Corporation [Freddie], the Federal National Mortgage Association [Fannie], or the Federal Home Loan Banks, or to honor, reimburse or otherwise guarantee any obligation…

But naturally, when push came to shove in the housing-finance crisis, the federal government, directly and indirectly, did fully honor, entirely reimburse and effectively guarantee all the obligations of Fannie and Freddie anyway.

The statute went on to say: