We Don’t Need GSEs

Testimony of

Alex J. Pollock

Resident Fellow

American Enterprise Institute

To the Committee on Financial Services

U.S. House of Representatives

Hearing on Learning from Mortgage Finance Systems of Other Countries

June 12, 2013

We Don’t Need GSEs

Mr. Chairman, Ranking Member Waters, and Members of the Committee, thank you for the opportunity to be here today. I am Alex Pollock, a resident fellow at the American Enterprise Institute, and these are my personal views. Before joining AEI, I was the President and CEO of the Federal Home Loan Bank of Chicago from 1991 to 2004. From 1999 to 2001, I also served as President of the International Union for Housing Finance (IUHF), a trade association devoted to the international exchange of housing finance ideas and information. In fact, I have just returned to the U.S. from an IUHF conference at which representatives of 42 countries met to share issues and experiences in this sector, which is economically and politically important to all countries.

The American housing finance sector has collapsed twice in the last three decades, once as a government promoted savings and loan-based system, and once as a government promoted GSE-centric system. We should never assume that the particular, highly unusual, historical development of U.S. housing finance should define the limits of our considerations. There is no doubt that there is much to learn of much practical import from examining U.S. housing finance in international perspective, including how experts from other countries view our system from outside.

Comparing our housing finance sector to other countries, the one thing most unusual about it was and is the dominant and disproportionate role played by Fannie Mae and Freddie Mac, as government-sponsored enterprises or GSEs. Fannie and Freddie’s role and was and is unique among housing finance systems. The GSEs themselves used to claim that this made U.S. housing finance “the envy of the world,” a view not shared by the world. When Fannie and Freddie were the darlings of Washington and the stars of Wall Street, they would come to IUHF meetings and boastfully promote their GSE model. But mortgage professionals from other countries were not convinced.

Let us begin by asking and answering five essential questions from an international perspective:

1. Are GSEs like Fannie and Freddie necessary for effective housing finance?

No. This is obvious from the many countries which achieve similar or higher home ownership than the U.S. without them.

2. Did GSEs get for the U.S. an internationally high home ownership rate?

No.

3. Well, did GSEs get for the U.S. an above-average home ownership rate?

No.

4. Are GSEs necessary to have long-term, fixed rate mortgages?

No.

5. Even if they had a disastrous actual outcome, are GSEs the best model in theory?

No.

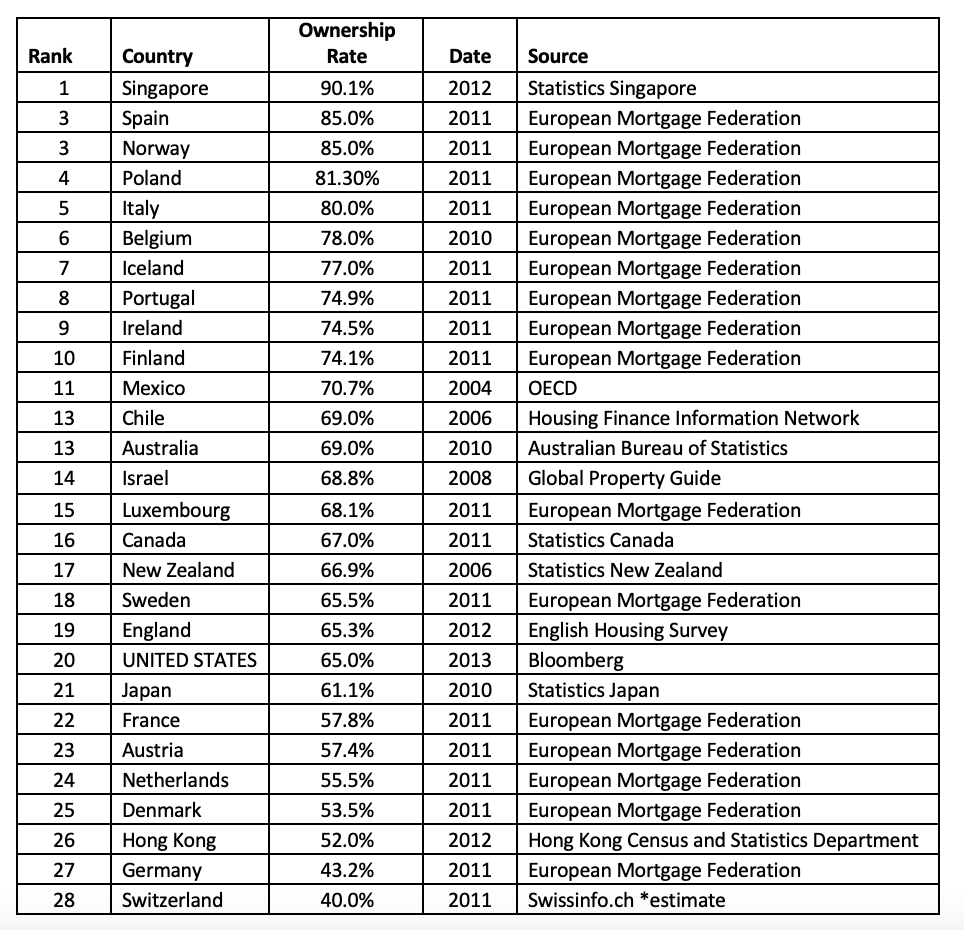

Along with incorrectly saying that GSEs made U.S. housing finance “the envy of the world,” it was often additionally claimed (without supporting data) that the U.S. had the highest home ownership rate in the world. This seemed plausible to Americans, but was wrong. Interestingly, people in England also claimed that they had the highest home ownership. In fact, England, with a completely different housing finance system and no GSEs, has been and is effectively tied with the U.S. in home ownership rate—both now at 65%, and both in the bottom half, as you will see in the ranking below.

Based on the free use of the U.S. Treasury’s credit, through the so-called “implicit” but very real (as events made clear) guaranty, massive amounts of Fannie and Freddie’s debt securities were sold around the world. The GSEs ran up the leverage of the housing finance sector. As a market distortion which pushed credit at housing, they inflated house prices and escalated systemic risk. Foreign investors helped pump up the housing bubble through the GSEs while being fully protected from the risk, and then were bailed out by the taxes of ordinary Americans. Of course, other countries also made housing finance mistakes, but nobody else made this particular, giant mistake.

The political interest in housing finance begins with what I think is a valid proposition: that in a democracy it is advantageous to have widespread property ownership among the citizens. The experiences of other countries make it obvious that high home ownership levels can be attained without GSEs—and moreover without tax deductions for mortgage interest; without our very unusual practice of making mortgage loans into non-recourse debt; without government orders to make “creative”—that is riskier—mortgage loans, which were part of being a GSE; and with prepayment fees.

The following table, “Comparative Home Ownership Rates,” is an update with the most recent available data of a comparison I presented to the Congress in 2010. It displays home ownership in 28 economically advanced countries. The U.S. ranks 20th, just behind England. The median home ownership rate among these countries is 68%, compared to our 65%.

Comparative Home Ownership Rates

Source: AEI research

How do financial professionals in other countries view the U.S. housing finance sector?

More than a decade ago, when Fannie and Freddie were still riding high, and Fannie in particular was a greatly feared bully boy whom both Washington politicians and Wall Street bankers were afraid to cross or offend, I presented the GSE-centric U.S. housing finance system to the Association of Danish Mortgage Banks in Copenhagen. When I was done, the CEO of one of their principal mortgage lenders memorably summed things up:

“In Denmark we always say that we are the socialists and America is the land of free enterprise. Now I see that when it comes to mortgage finance, it is the opposite!”

He was so right. But now, with Fannie and Freddie continuing to be guaranteed by the U.S. Treasury, able to run with zero capital and infinite leverage, being granted huge loopholes by the Consumer Financial Protection Bureau, and being heavily subsidized by the Federal Reserve’s buying up their MBS, they have a bigger market share and more monopoly power than before. The American housing finance sector is more socialized than ever.

Here’s a view from Britain, where a senior financial official said recently:

“We don’t want a government guaranteed housing finance market like the United States have.”

They don’t want what we have—and we don’t want it either. How do we conceptualize the range of alternate possibilities?

Every housing finance system in the world must address two fundamental questions. The first is how to match the nature of the mortgage loan with an appropriate funding source, so you are not lending long and borrowing short. Different approaches distribute the interest rate risk among the parties involved—lenders, investors, borrowers, governments, taxpayers--in various ways.

Basic sustainable variations observed in different countries include variable rate mortgages funded with short-term deposits; medium term fixed-rate mortgages funded with medium-term fixed rate deposits or bonds; long-term fixed rate mortgages funded with long-term fixed rate bonds or covered bonds. In general, to soundly fund long-term fixed-rate mortgages, you have to have access to the bond market. In an advanced financial system, it does not require a GSE to do this.

The classic example of not achieving the needed interest rate match was the collapse of the American savings and loan industry in the 1980s. What broke the savings and loans was the combination of their interest rate mismatch with the soaring interest rates of the great inflation created by the Federal Reserve in the 1970s. While the lenders were crushed, borrowers who had old 30-year fixed rate mortgages in this period of rising interest rates and inflating house prices did very well.

In contrast, the 30-year fixed rate mortgage was terrible for great numbers of borrowers in the U.S. crisis of the 2000s. With the floating rate mortgage system of England, the rapid fall of interest rates in the housing crisis was automatically passed on to the borrowers in the form of lower payments, which helped contain the crisis. American borrowers faced with falling interest rates and house price deflation, on the other hand, were often locked in to high payments and punished by their 30-year fixed rate mortgages, which thereby made the housing bust worse in this country.

The second fundamental question of housing finance systems is who will bear the credit risk. In most countries, the lender retains the credit risk, which is undoubtedly the superior alignment of incentives. With covered bonds, which are used in many countries, you can simultaneously achieve fixed-rate funding while keeping the lender fully on the hook for the credit performance of the mortgage loans being funded.

The American GSE approach (and also that of private MBS) systematically separates the credit risk from the lender-- so you divest the credit risk of the loans you make to your own customers. This was and is a distinct outlier among countries. It had disastrous results, needless to say.

The most perfect conceptual solution to the two fundamental questions of housing finance, which functions very well in practice in its national setting, is the housing finance system of Denmark. This system has been justifiably admired by many observers. It operates in a small country, but represents big basic ideas.

The Danish mortgage approach to interest rate risk in its funding market is explicitly governed by what it calls the “matching principle.” This means that the interest rate and prepayment characteristics of the mortgage loans being funded are passed on entirely to the investor in Danish mortgage covered bonds. This allows long-term fixed rate mortgages, as well as variable rate mortgages.

At the same time, the entire credit risk is retained by the mortgage bank lenders. They have 100% “skin in the game” for credit risk, in exchange for an annual fee, thus insuring alignment of incentives for credit performance. Deficiency judgments, if foreclosure on a house does not cover the mortgage debt, are actively pursued. In other words, mortgage loans are always made with recourse to the borrower’s other income and assets. This is true in most countries. The U.S. state laws or practices of non-recourse mortgage lending are again a distinct outlier.

The fundamentals of the Danish mortgage system go back over 200 years, to the 1790s. There are no GSEs. The Danish system can deliver long-term fixed rate loans of up to 30 years with a prepayment option. This is a private housing finance system build on quite robust principles, which claims that no mortgage bond holder has suffered a credit loss in over two centuries. Denmark can and in the last decade did have a housing price bubble and bust, but the housing finance sector performed much better through it than did ours, and its covered bonds were sold throughout 2007-09. We should note that the Danish system generates a home ownership rate of 54%, on the low side.

Another interesting case of the splitting of bond market funding and credit risk is that of Cagamas, or the National Mortgage Company of Malaysia. Cagamas buys mortgage loans from lenders, and then issues bonds to finance them, but the mortgage purchases are with full recourse to the lender, so the lender retains 100% of the credit risk and the alignment of incentives.

Cagamas is 80% owned by the banks and 20% by the Malaysian central bank, so it is a GSE, but not a Fannie and Freddie-style GSE. Instead it functionally resembles the Federal Home Loan Banks (FHLBs). FHLBs provide bond market funding for mortgages through advances to banks, but the banks retain all the credit risk. FHLBs also buy mortgages, but only when the bank credit enhances the mortgages it has made. (It may be of interest that of all sizeable American GSEs, considering Fannie, Freddie and the Farm Credit Banks, the FHLBs are the only ones which have never gone broke.)

A very stable, sound, and very conservative housing finance market is that of Germany. Some of its banks got into trouble in this cycle by buying U.S. mortgage securities, but their domestic mortgage market did not experience either a housing price boom-bust or a mortgage credit crisis. The problem is that the German system generates a very low home ownership rate, only 43%--as well as a relatively late age at which people are on average able to buy houses. I imagine that neither of these would be politically acceptable in the U.S.

Nevertheless, there are two German ideas worthy of study. One is the German version of mortgage covered bonds (“Pfandbriefe”). With a statutory basis more than one hundred years old (and, it is claimed, a history going back to Frederick the Great in the 18th century), these covered bonds form and large and relatively stable source of bond-based mortgage funding with no GSE. The issuing bank retains all the credit risk of the mortgage loans. Mortgage loans funded with these covered bonds have a maximum LTV of 60%.

Many people have proposed, and I agree, that the U.S. should introduce covered bonds without a government guaranty as a mortgage funding alternative, as part of escaping from the mortgage market’s subservience to GSEs.

A second German housing finance idea worth considering is their emphasizing the role of savings as an essential part of sound housing finance. The German building and savings banks (“Bausparkassen”) continue to practice the savings contract, which was once also common in this country. By such a contract, the borrower commits to regular savings as part of qualifying for a mortgage loan. This is, in my opinion, a very old-fashioned, very good idea.

Canada makes a pertinent comparison for the U.S., both countries being advanced, stable, financially sophisticated and North American. The Canadian housing finance system, like most in the world, has no GSEs. It is primarily funded on the balance sheets of banks, although Canadian banks are also becoming issuers of covered bonds under new legislation, and it came through the crisis of 2007-09 in much better shape than did we did. Mortgage lending is more conservative and creditor-friendly, and the Canadian system currently produces a higher home ownership rate of 67%.

Although it has no GSEs, Canada does have a very important government body to promote housing finance, which plays a substantial role in the mortgage sector. This is the Canada Mortgage and Housing Corporation (CMHC). Its principal activity is insuring (i.e. guaranteeing) mortgage loans—and it guarantees approximately half of all Canadian mortgages. This is about the same proportion as the combined Fannie and Freddie have of outstanding the U.S. mortgage credit exposure.

But in contrast to the game the U.S. played of pretending that Fannie and Freddie were “private,” and that the government exposure was not really there (it was only “implicit”), CMHC’s status is refreshingly clear and honest. It is a 100% government-owned and controlled corporation. It has an explicit guaranty from the government. It also provides housing subsidies which are on budget and must be appropriated by Parliament. So Canada, while having this large government intervention in the mortgage market, is definitely superior to us in candor and clarity about it.

This exemplifies what I believe to be a core principle: You can be a private company. Or you can be part of the government. But you should never be allowed to pretend you are both. In other words, Fannie and Freddie should cease to be GSEs. Considering the international anomaly and the disastrous government experiment they represent, we should all be able to agree on this.

Thank you again for the opportunity to share these views.